Connect on LinkedIn

Connect on LinkedInWhile you may never have filed it while living within the United States, Form 1116 is a key component of many US expat tax returns. This form allows you to claim the Foreign Tax Credit (FTC), one of the most important tax breaks for Americans living abroad.

For many expats, the Foreign Tax Credit (FTC) significantly reduces or even eliminates their US tax bill, and any unused credits can still be carried forward for up to 10 years or back for one year. Given how much is at stake, it’s critical to complete and file Form 1116 correctly. That said, it’s not exactly the most straightforward form.

The good news? We’re here to explain it to you. As a dedicated US expat tax firm, at Bright!Tax we know Form 1116 inside and out. Below, we’ll go over what exactly the FTC is, how it works, how to file Form 1116 step by step, and more.

Key Updates for 2025

- The IRS has released the 2025 version of Form 1116, incorporating updates to reflect current tax laws and regulations.

- Taxpayers must adjust foreign qualified dividends and capital gains on Form 1116, line 1a, using specific factors based on U.S. tax rates.

- The IRS emphasizes the requirement to apportion all interest expenses between U.S. and foreign source income on Form 1116, lines 4a and 4b.

Understanding the Foreign Tax Credit (FTC)

Before we dive into the specifics of Form 1116, let’s delve into the FTC in a bit more detail.

What is the FTC?

The FTC is a tax break that gives Americans dollar-for-dollar US tax credits for any foreign income taxes they’ve paid. In essence, this lets you use your foreign tax bill to offset your US tax bill (although as we’ll go into later, it’s a bit more complex than that).

If you live in a country with higher tax rates than the US, you may eliminate your US tax bill entirely using the Foreign Tax Credit, with any excess credits available for future use. You can then apply these credits to tax bills from one year prior, or up to ten years in the future.

FTC qualifications

To qualify for the Foreign Tax Credit, foreign taxes must be:

- Legal

- Paid or accrued

- Income-based

- Payable by you specifically

Taxes on certain types of income are ineligible for the FTC, such as:

- Social Security taxes

- Value-added taxes (VAT)

- Income that is already eligible for exclusion or deduction

FTC limits

The IRS still enforces an FTC limit to prevent the credit from offsetting taxes on US-sourced income, but recent clarifications affect how passive income is treated.

Example: Rosa is a dual US/Peruvian citizen who works remotely, spending ⅓ of her time in the US and the other ⅔ in Peru at her grandmother’s home. She earned $90,000 in tax year 2025 — $60,000 while in Peru, and $30,000 while in the US. Her total US tax liability before applying the FTC is $11,983.

She must calculate her FTC limit as follows:

- Divide foreign-earned income ($60,000) by worldwide income ($90,000): ⅔, or roughly 0.67

- Multiply this figure (0.67) by her US tax liability ($11,983): $7,989

Therefore, Rosa can claim no more than $7,989 in US tax credits under the FTC.

Another limitation of the FTC is the high-tax kickout, which limits how much the FTC can reduce US tax liability when foreign passive income is taxed at a much higher tax rate than the top US rate. The IRS has clarified that passive income taxed at a rate exceeding 90% of the highest US tax rate may be subject to the high-tax kickout, limiting its eligibility for the FTC.

When to file Form 1116

Individuals who want to claim the FTC must almost always file Form 1116. Corporations, on the other hand, will file Form 1118.

However, there are a few specific situations in which you can claim the FTC without filing the corresponding form. In this case, the typical FTC limit won’t apply to you either.

If you meet all three of the following conditions, you can claim the FTC without filing Form 1116:

- All of your foreign source gross income is classified as passive income, high-taxed income, or export financing interest, AND

- All of the income and foreign taxes you paid on it were reported on a qualified payee statement like Form 1099-DIV, Form 1099-INT, Schedule K-1 (Form 1041), Schedule K-3 (Form 1065), Schedule K-3 (Form 1120-S), or similar statements, AND

- Your foreign taxes do not exceed $300 (or $600 if you’re filing jointly)

Note:

This excludes estates and trusts.

To claim the FTC in this scenario, you’ll enter the credit in the appropriate field on your primary tax return (usually Form 1040).

Step-by-step guide to completing Form 1116

Now that you better understand what the FTC is and how it works, let’s get into how to complete Form 1116.

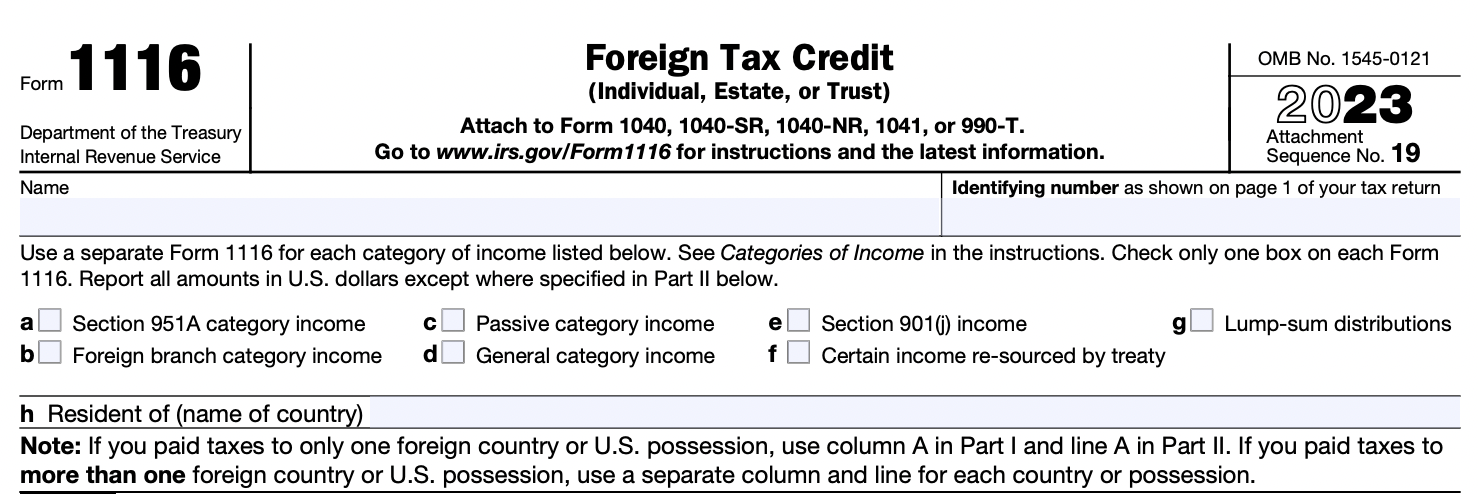

Up top, you’ll disclose your name, identifying number (usually your Social Security Number, or SSN),the income type you’re filing Form 116 for, and your country of residence.

Note that there are seven different income categories:

- Section 951A category income: Refers to Global Intangible Low-Taxed Income, aka GILTI

- Foreign branch category income: Refers to income earned through a foreign branch of a US company

- Passive category income: Refers to unearned income like royalties, rent, interest, and dividends

- General category income: Typically refers to income earned through foreign business operations or services, provided that it does not fit into any of the other income categories

- Note: This will be the main category relevant to most US expat employees and business owners.

- Section 901(j) income: Refers to income earned from sanctioned countries or those with discriminatory tax systems

- Certain income re-sourced by treaty: Refers to income that is treated as if it came from a different country than where it was earned due to a tax treaty

- Lump-sum distributions: Refers to single, one-time payments, typically related to pensions and retirement plans

Each of these are taxed differently, so it’s critical to know which category your income falls into. Thorough documentation of your income throughout the year will help make this process easier. And remember — you must use a different Form 1116 for each income category.

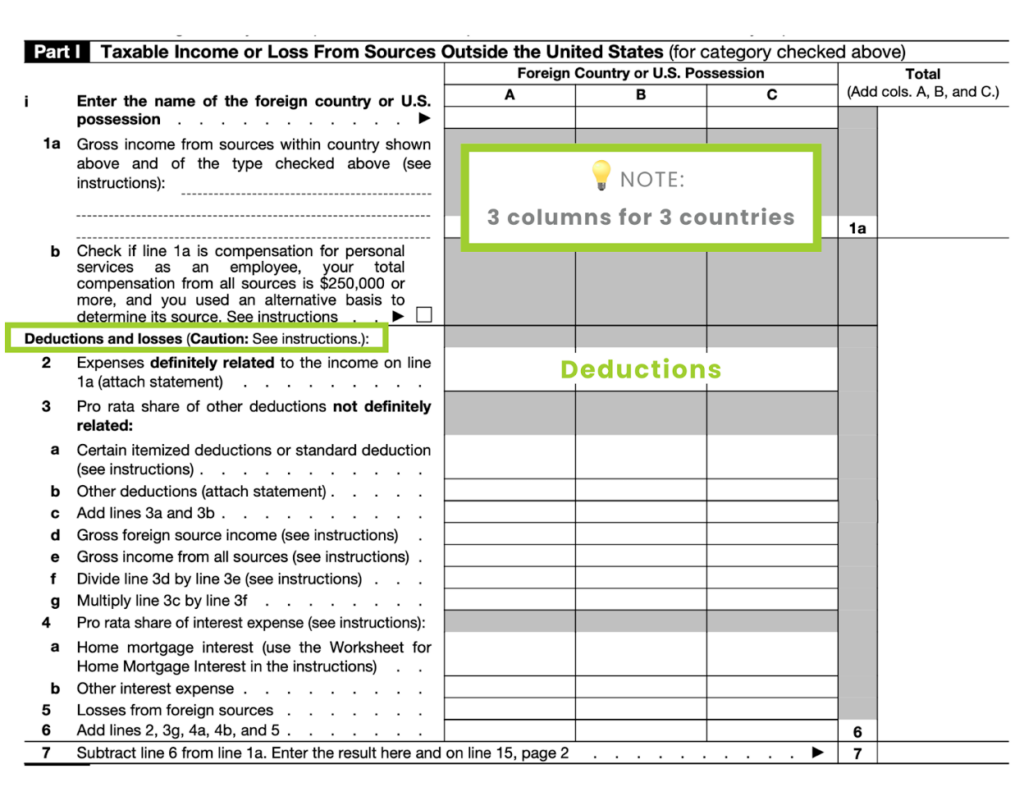

Part I: Taxable Income or Loss from Sources Outside the United States

In this section, you’ll record all income from foreign sources. If you’ve paid taxes in more than one foreign country, you must allocate the income across columns A, B, and C accordingly. If you paid taxes in more than three countries, you must attach a separate sheet with a similar format to Part 1 (but not an extra copy of Form 1116).

Tips:

- Include all foreign income, even if all or some is not taxable by a foreign government

- Convert all foreign currency into US dollars using a reliable source

- Note: When converting currency in your tax return, you must include a statement showing the IRS how you made your calculation

- Adjust gross income (line 1a) for any foreign income that you’ve excluded with Form 2555 (aka the Foreign Earned Income Exclusion, or FEIE)

You’ll also need to input the amount in deductions you used to reduce your taxable income. This can include either the standard deduction or itemized deductions (e.g. home mortgage interest, foreign-sourced tax losses).

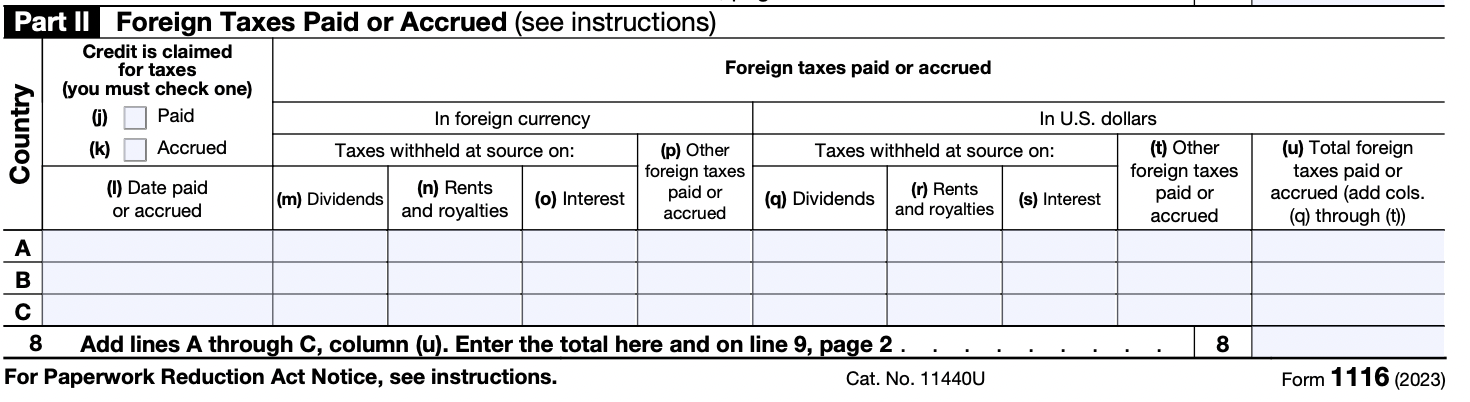

Part II: Foreign Taxes Paid or Accrued

In Part II, you’ll describe the amount of foreign tax you either paid or accrued in the current tax year on the income you reported in Part I.

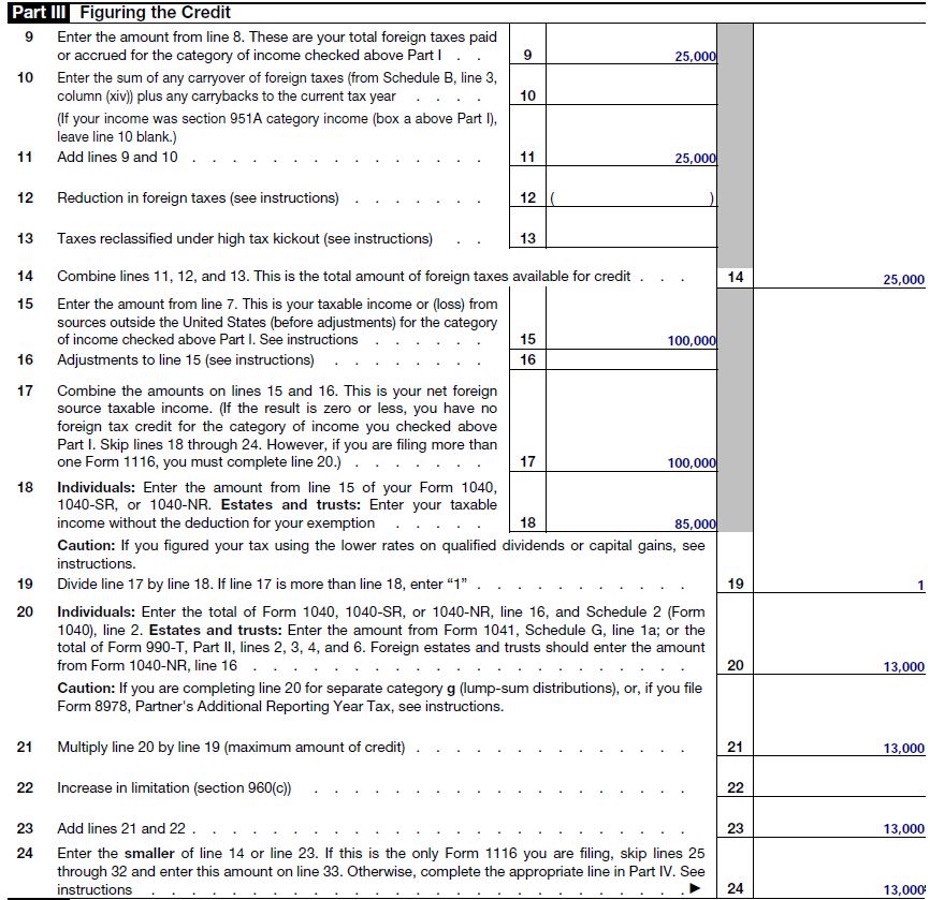

Part III: Figuring the Credit

In this section, you’ll calculate your personal Foreign Tax Credit. This won’t necessarily be equal to the amount you paid in taxes in your country of residence, however. Instead, it’s the amount of tax you would have paid if the income had been earned and taxed according to the US tax code.

We’ve filled this section out to illustrate a hypothetical scenario:

1️⃣ Let’s say you work in Italy, where you earned an annual salary equivalent to $100,000 in 2023. Your Italian tax payment, meanwhile, came out to $25,000. Remember, though, that this isn’t equal to the amount you can claim under the FTC.

2️⃣ Your total deductions for the year were $15,000 — therefore, your taxable income is $85,000 ($100,000 – $15,000).

3️⃣ Finally, let’s assume that your US tax liability for $85,000 would be $13,000. This is the amount that you can apply toward your US tax bill, NOT the $25,000 you paid in Italy.

| Annual Salary | $100,000 |

| US Tax Deductions | ($15,000) |

| US Taxable Income | $85,000 |

| US Tax | $13,000 |

| Italian Taxes | $25,000 |

| Foreign Tax Credit | $13,000 |

Part IV: Summary of Credits from Separate Parts III

In the last section, you’ll calculate your total Foreign Tax Credit by adding up the credits for each individual income category and making adjustments as necessary.

Other expat tax benefits

While the FTC can be a powerful tax break for US expats, it’s not the only one available. A couple of other expat-specific tax breaks include the:

Foreign Earned Income Exclusion (FEIE)

The Foreign Earned Income Exclusion, or FEIE, lets expats exclude a certain amount of their foreign-earned income from taxation. Note that this does not include unearned/passive income like income from rental properties, dividends, interest, or pension income. The Foreign Earned Income Exclusion (FEIE) limit for 2025 has increased to $130,000, reflecting adjustments for inflation.

To be eligible for the FEIE, you must meet one of two tests:

- The Physical Presence Test: Be physically present outside the US for at least 330 days in a 365-day period overlapping the tax year

- The Bona Fide Residence Test: Have resided in another country for at least the entire tax year and be able to prove it through official documentation (ID cards, rental contract, utility bills, etc.) if necessary

If you qualify, you can claim the FEIE by filing Form 2555.

How the FTC interacts with the FEIE

One big caveat to keep in mind is that you cannot apply the FEIE and the FTC to the same income. You can, however, apply them to separate items of income.

Example: Jonah lives in Canada, where he earns a salary equivalent to $80,000 US dollars. He also rents out a room in the apartment that he owns in Vancouver for $850 (USD) per month — an annual total of $10,200. Jonah excludes his entire salary under the FEIE, and claims the FTC on the taxes he has paid on rental income in Canada.

Foreign Housing Exclusion or Deduction FHE/FHD

If you qualify for the FEIE, you also automatically qualify for the Foreign Housing Exclusion (if you’re an employee) or Foreign Housing Deduction (if you’re self-employed). Both of these may help you offset the cost of certain foreign housing costs, like rent, utilities, parking, and more.

Just as with the FEIE, you cannot claim the FTC on the same income you’ve applied the FHE/FHD to. To claim the FHE/FHD, you’ll use the same form as the FEIE: Form 2555.

Frequently Asked Questions (FAQs)

-

What is Form 1116?

Form 1116 is used by U.S. taxpayers to claim the Foreign Tax Credit, which helps prevent double taxation on income earned abroad.

-

Who should file Form 1116?

U.S. citizens or residents who have paid or accrued foreign taxes on income that is also subject to U.S. tax should file Form 1116 to claim the credit.

-

How do I adjust foreign qualified dividends and capital gains?

You must adjust these amounts on Form 1116, line 1a, by applying specific factors based on the U.S. tax rate applicable to the income.

-

What are the rules for apportioning interest expenses?

All interest expenses must be apportioned between U.S. and foreign source income, regardless of where the loan was obtained, and reported on Form 1116, lines 4a and 4b.

-

Where can I find the latest Form 1116 and instructions?

The most recent version of Form 1116 and its instructions are available on the IRS website.