Connect on LinkedIn

Connect on LinkedInNearly a third of Americans say they would like to move overseas if they had the opportunity to do so. While moving abroad can be the adventure of a lifetime, it can complicate your United States tax and reporting obligations. Case in point: FinCEN Form 114, also known as the Foreign Bank Account Report (FBAR).

Many Americans abroad must file the FBAR. And unfortunately, failing to do so when you meet the filing requirements can lead to major penalties. The good news? As a US expat tax firm, we’re here to walk you through it step by step.

Below, we’ll go over everything US expats need to know about the FinCEN 114 Form. Read on to learn who has to file this form, how to fill it out, when to submit it, and more.

What is FinCEN Form 114 (FBAR)?

FinCEN Form 114: the Report of Foreign Bank and Financial Accounts is a mandatory report for expats whose foreign financial account holdings exceed a certain threshold. More commonly known as the FBAR, FinCEN 114 is used to report the content of your financial accounts held with banks and other financial institutions outside the US.

Note:

Foreign financial account refers to an account held at, in, or through a financial institution based in a foreign country. You don’t need to disclose your US-based accounts on an FBAR, even if they contain foreign assets.

Unlike the vast majority of forms associated with US tax and reporting obligations, this form is filed with the Financial Crimes Enforcement Network (FinCEN), a department of the US Treasury, rather than the Internal Revenue Service (IRS). While the overwhelming majority of FBAR filers are law-abiding expats, the FBAR does help prevent a few bad actors from engaging in tax evasion, money laundering, and other financial crimes.

Who is required to file FinCEN Form 114?

The FBAR is a mandatory report for American taxpayers whose foreign financial account holdings exceed $10,000 at any time during the tax year. Note that this figure includes the total across all foreign financial accounts, not just the value of one account.

Let’s say, for example, that you hold a bank account in Panama with $5,000 in it and a brokerage account in Mexico worth $6,000. Even though neither account surpassed $10,000 individually, the total of the foreign financial accounts exceeds $10,000. Thus, you are required to report the contents of these accounts on the FBAR.

Tip:

While those who surpass the FBAR threshold must file FinCEN Form 114, the FBAR does not in itself levy a tax on the foreign financial holdings.

It’s also important to mention that these accounts do not necessarily need to be in your name for you to report them. Accounts over which you, or a business you own, have control or signatory authority count as well.

A few types of foreign financial accounts subject to the FBAR include:

- Bank accounts

- Brokerage accounts

- Mutual funds

- Business accounts

- Cryptocurrency accounts on foreign exchanges

- Insurance policies with a cash value

A few types of non-reportable foreign financial accounts include:

- US accounts containing foreign assets

- Correspondent or Nostro accounts

- Accounts owned by governmental entities

- Accounts owned by a foreign financial institution

- Accounts maintained in a US military banking facility

- Individual retirement accounts (IRAs)

FinCEN Form 114 vs. Form 8938

US expats sometimes confuse the FBAR/FinCEN Form 114 with Form 8938: the Statement of Specified Foreign Financial Assets. While both reports deal with disclosing foreign financial holdings to prevent financial crime, there are several major differences.

The assets subject to reporting on Form 8938 include both foreign financial accounts as well as:

- Foreign stocks & securities

- Foreign government bonds

- Shares in a foreign business

- Foreign trusts & estates

- Foreign derivatives

- Foreign real estate owned through a foreign entity

- Note: Foreign real estate that you own personally is exempt

Moreover, the reporting threshold for these assets is different. Americans must file Form 8938 if their relevant foreign financial assets exceed:

- $200,000 on the last day of the tax year, OR

- $300,000 at any time during the tax year

Note:

If you meet the reporting threshold for the FBAR as well as Form 8938, you must file both.

The FBAR has also been around longer than Form 8938. The FBAR became mandatory after the passage of the Bank Secrecy Act (BSA) in 1970. Form 8938, on the other hand, became mandatory after the passage of the Foreign Account Tax Compliance Act (FATCA) in 2010.

How to file FinCEN Form 114

To file FinCEN Form 114, you’ll go to the BSA E-Filing System on the FinCEN website. While the form is electronically filed regardless, you have two ways of doing so: by directly entering information on the FinCEN website, or by uploading a completed FBAR PDF form.

Either way, the report will be the same. However, the PDF will allow you to work at your own pace while entering your information requires you to submit in one go.

When to file FinCEN Form 114

FinCEN Form 114 is technically due on April 15th of a given calendar year. However, filers receive an automatic six-month extension until October 15th.

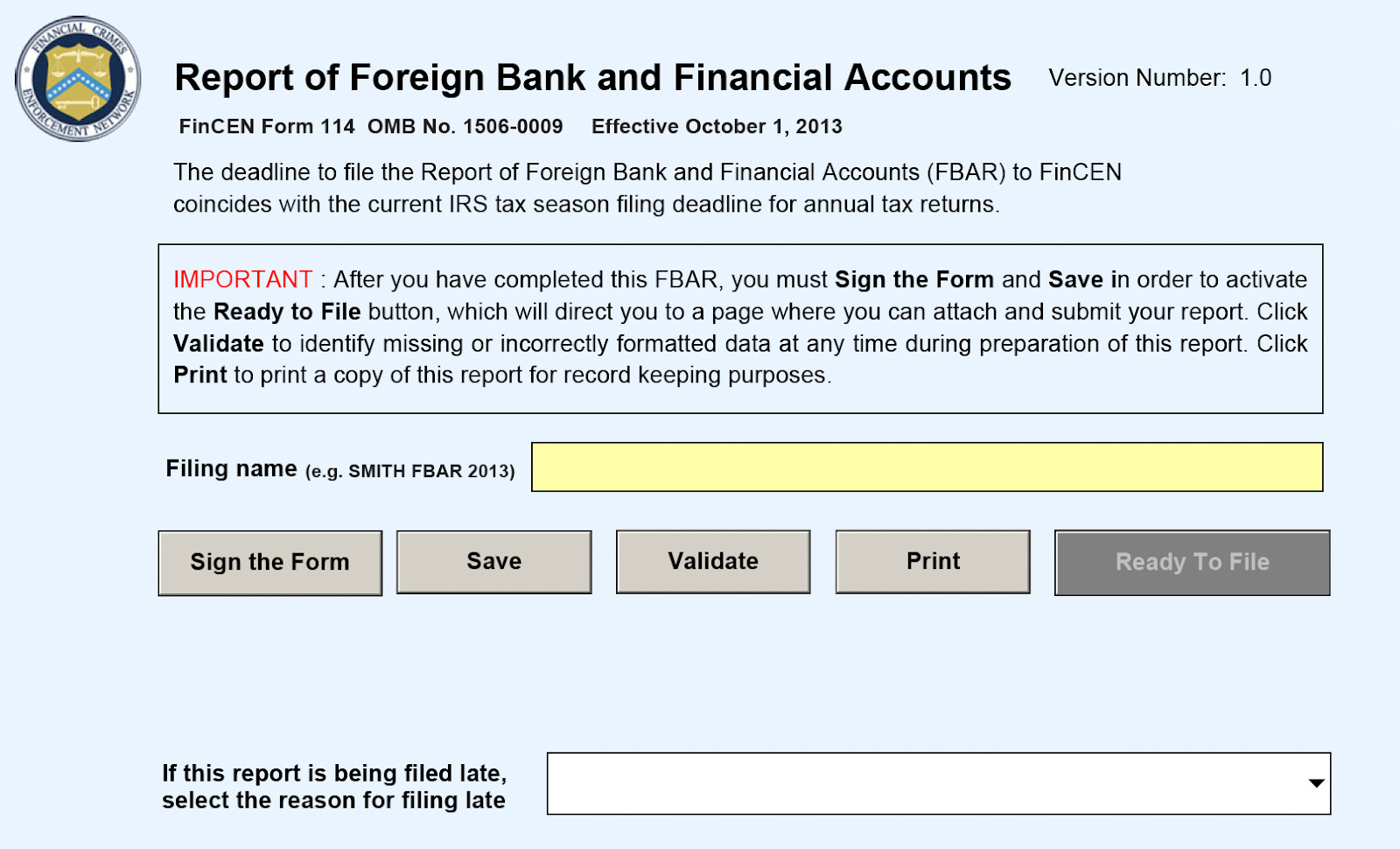

FinCEN Form 114 instructions, step by step

In the first part of the report, you’ll simply enter your last name, the name of the report, and the year (e.g. SMITH FBAR 2024). If you’re filing the report after the deadline, you’ll click on the dropdown menu to select the reason why it was late. You can choose from the following reasons:

- Forgot to file

- Did not know that I had to file

- Thought account balance was below reporting threshold

- Did not know my account qualifies as foreign

- Account statement not received in time

- Account statement lost (replacement requested)

- Late receiving missing required account information

- Unable to obtain joint spouse signature in time

- Unable to access BSA E-filing system

- Other

- Note: If you select this option, you’ll need to provide an explanation below

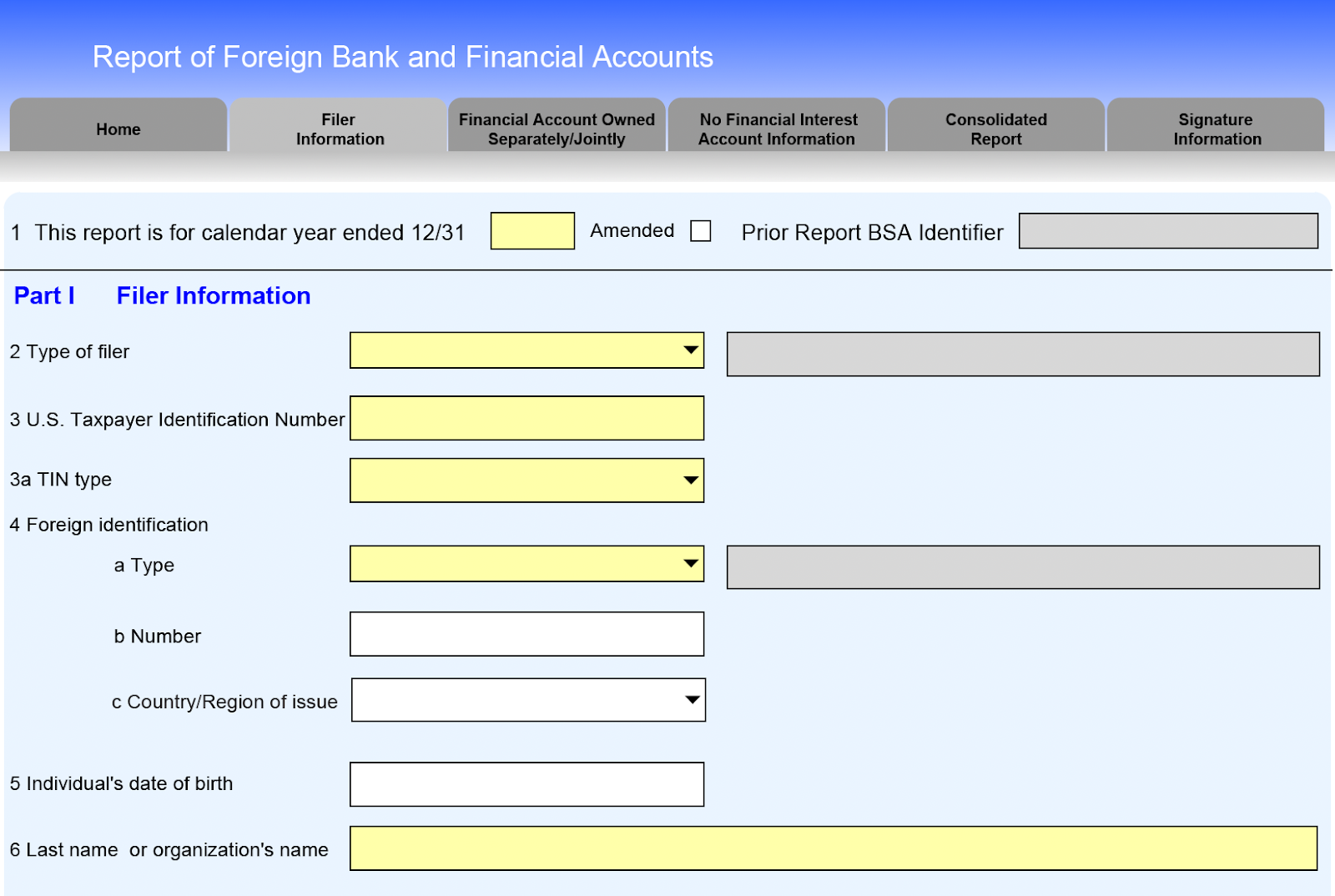

Part I: Filer Information

In this section, you’ll fill out some basic information about yourself, including:

- Your filing status

- Your Taxpayer Identification Number (TIN)

- Note: Most filers will enter their Social Security Number (SSN)

- Your date of birth

- Your full name

- Your address

At the end, you’ll check boxes to indicate whether you hold interest in or signature authority over 25 or more foreign financial accounts.

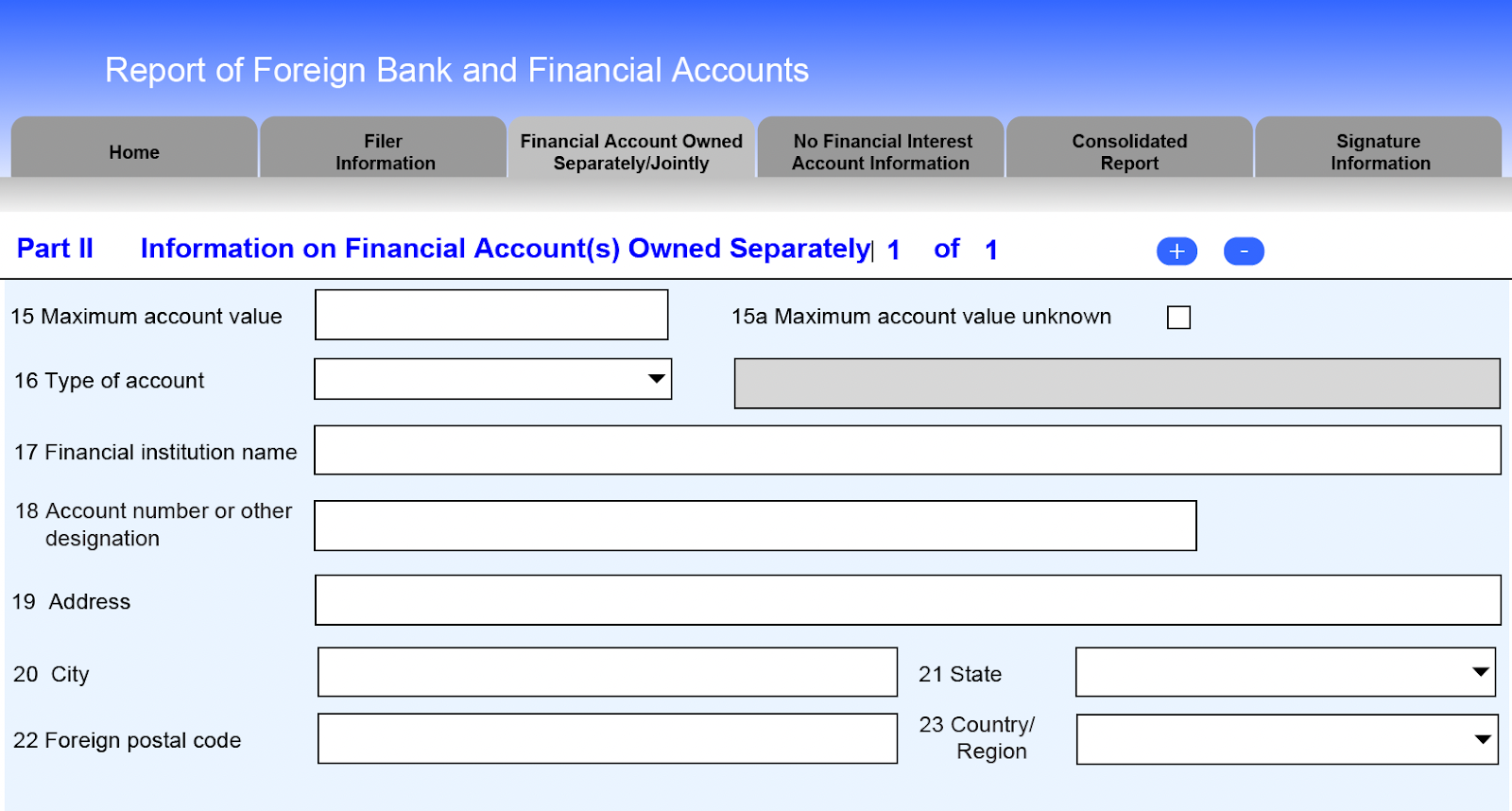

Part II: Information on Financial Account(s) Owned Separately

In Part II, you’ll need to share information on any financial accounts you own separately, including the:

- Maximum account value

- Type of account

- Name of the financial institution in which the account is held

- Account number

- Address of the financial institution in which the account is held

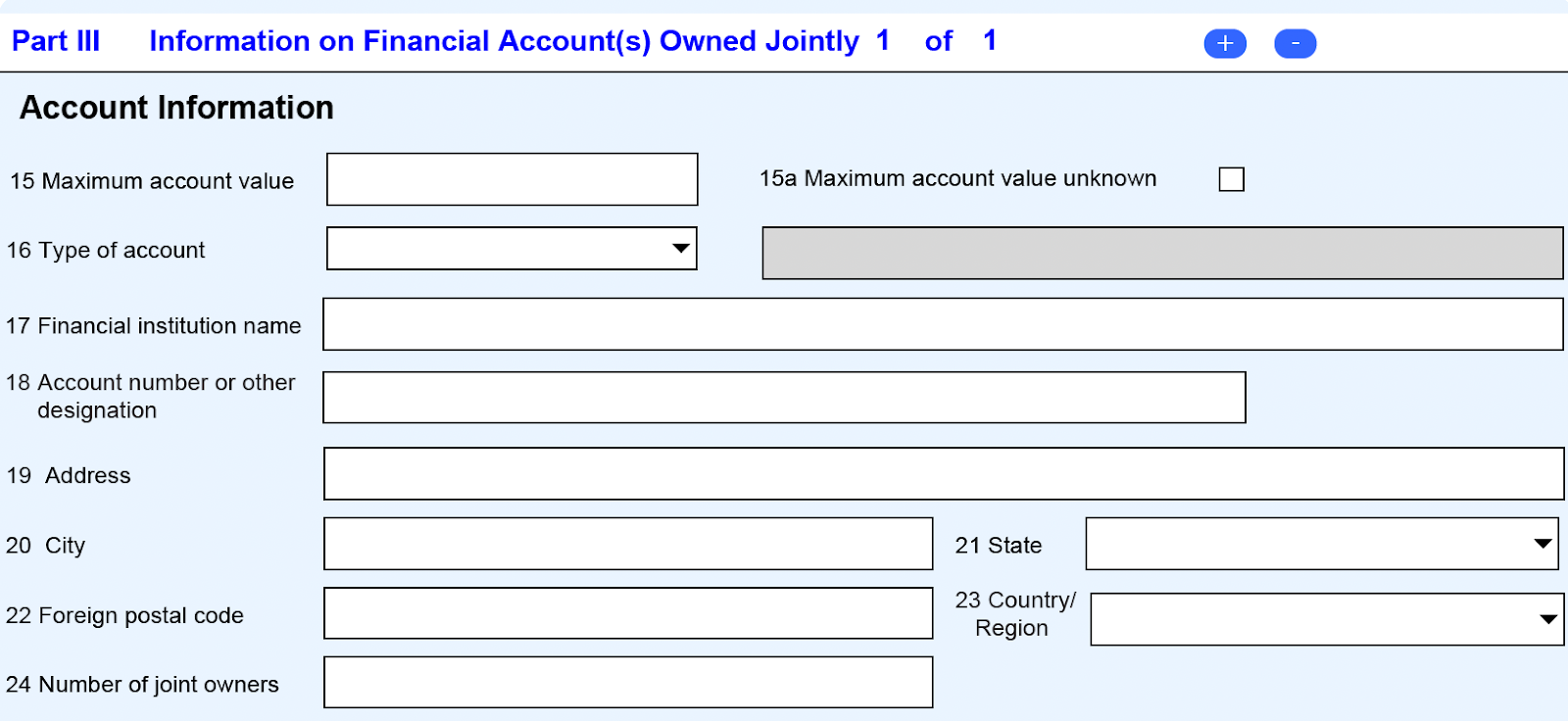

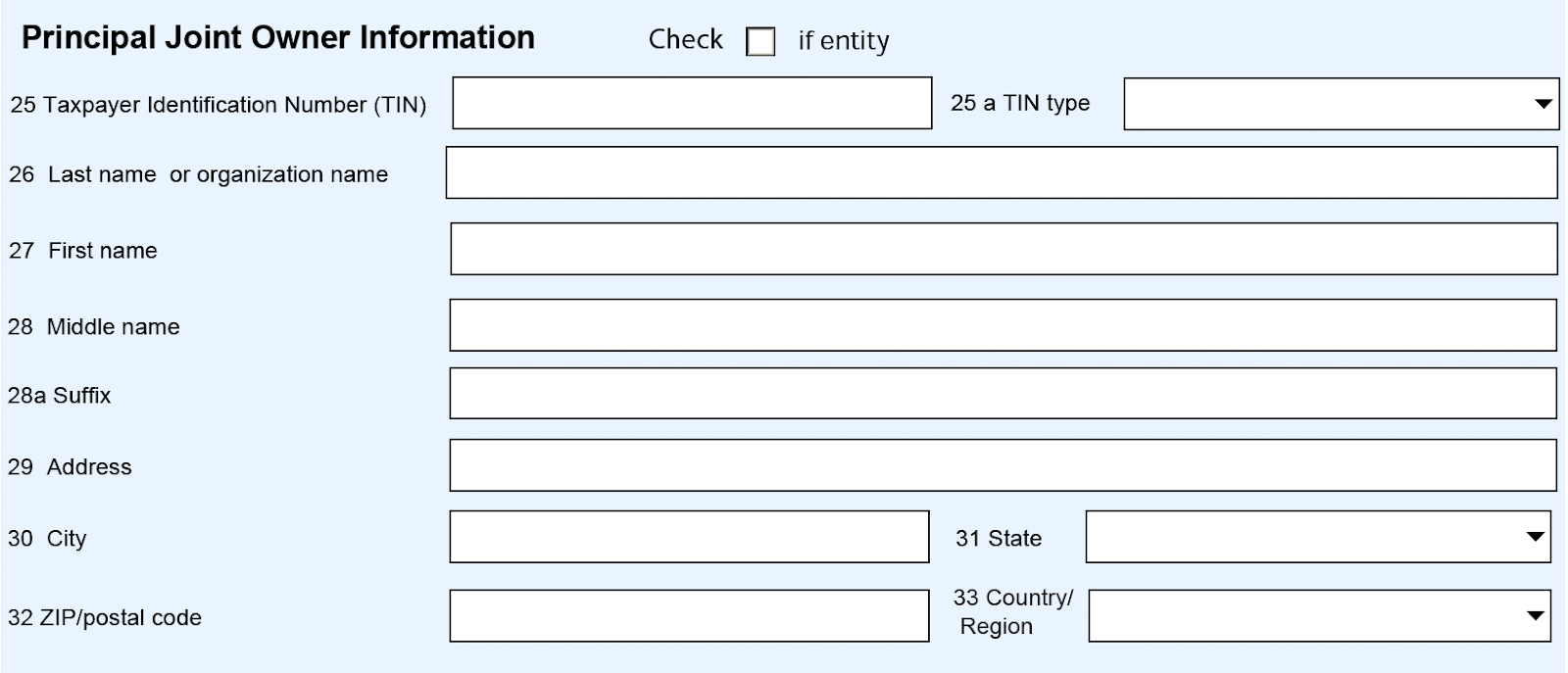

Part III: Information on Financial Account(s) Owned Jointly

In the first section of Part III, you’ll fill out the same type of account information you did before (e.g. account value, type of account, name of financial institution, address) for any accounts that you own jointly. In addition, you’ll state how many joint owners the account has.

In the second section of Part III, you’ll enter the name, TIN, and address of the principal owner of the joint account.

Tip:

If the principal owner is a US-based individual, you’ll select “SSN/ITIN” on the dropdown menu on 25a, Tin type. For US-based entities, you’ll select “EIN” (Employer Identification Number) under the dropdown menu. For foreign owners, you’ll select “Foreign.”

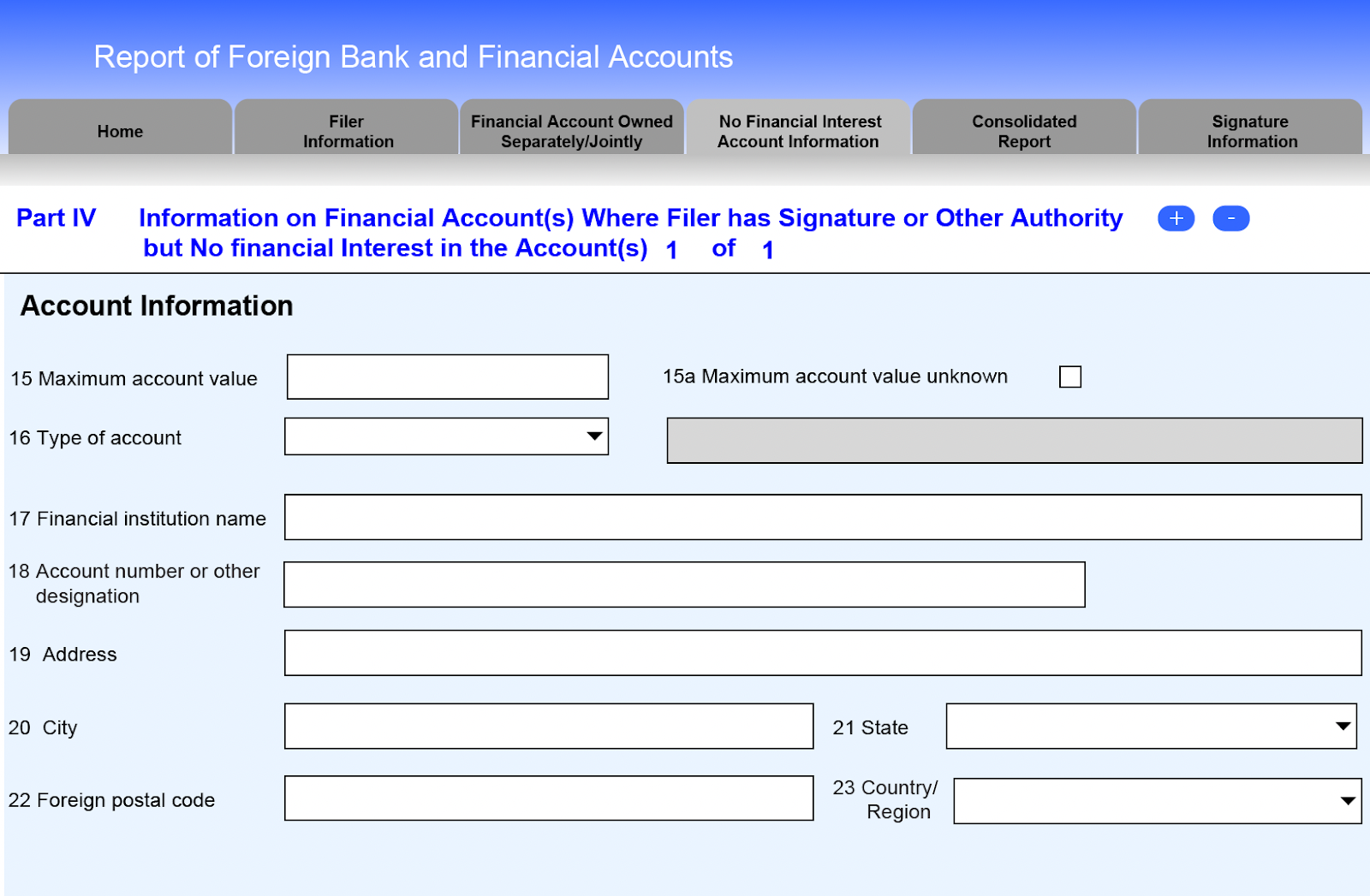

Part IV: Information on Financial Account(s) Where Filer has Signature or Other Authority but No financial Interest in the Account(s)

In Part IV, you’ll share account information for financial accounts over which you have signatory authority, but no financial interest in. This might include something like a business bank account, where you can access or manage the account but not directly withdraw or benefit from the funds within it.

Then, you’ll share information about the owner, making sure to check the box up top if the owner is an entity like a business or trust.

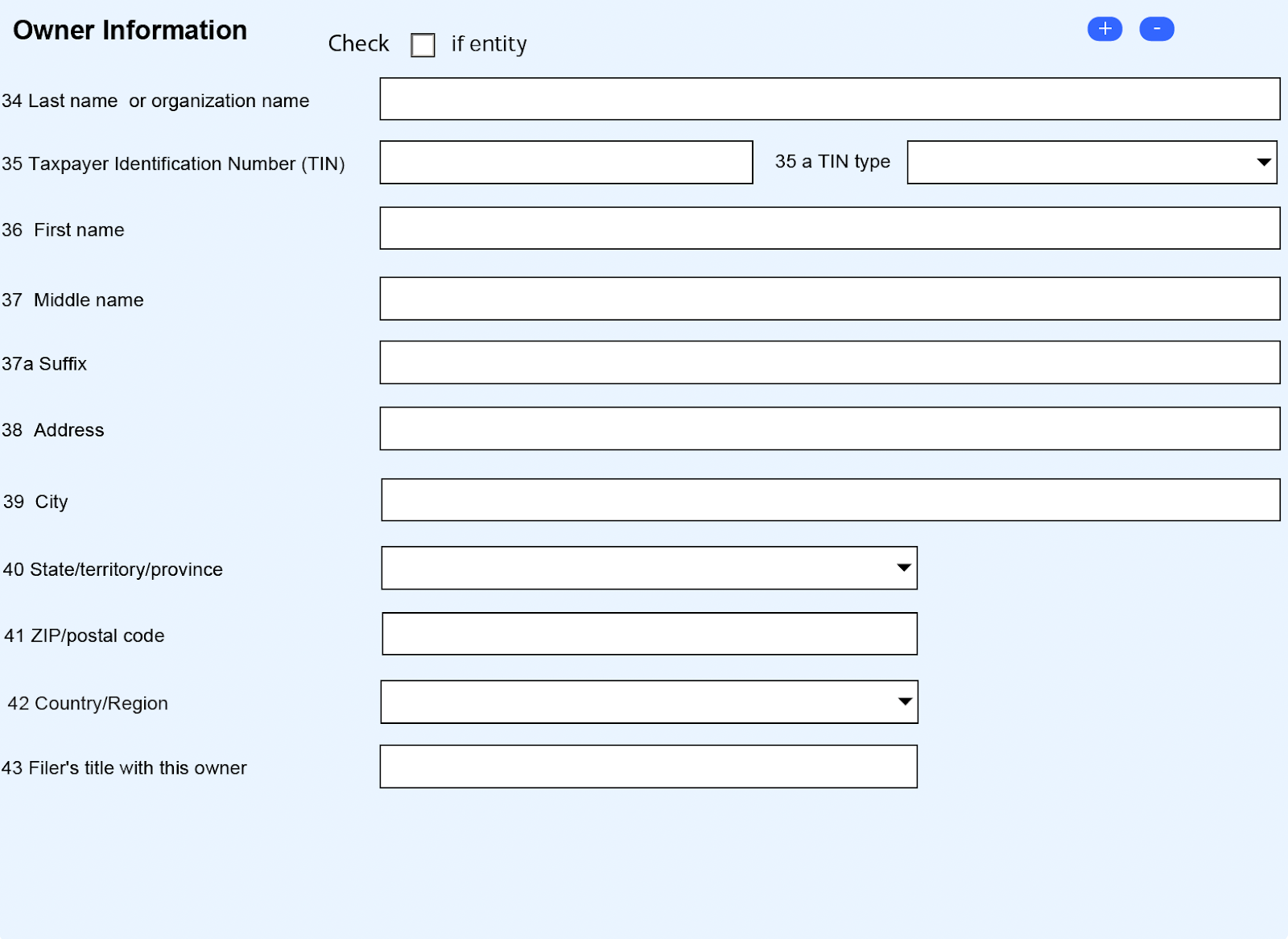

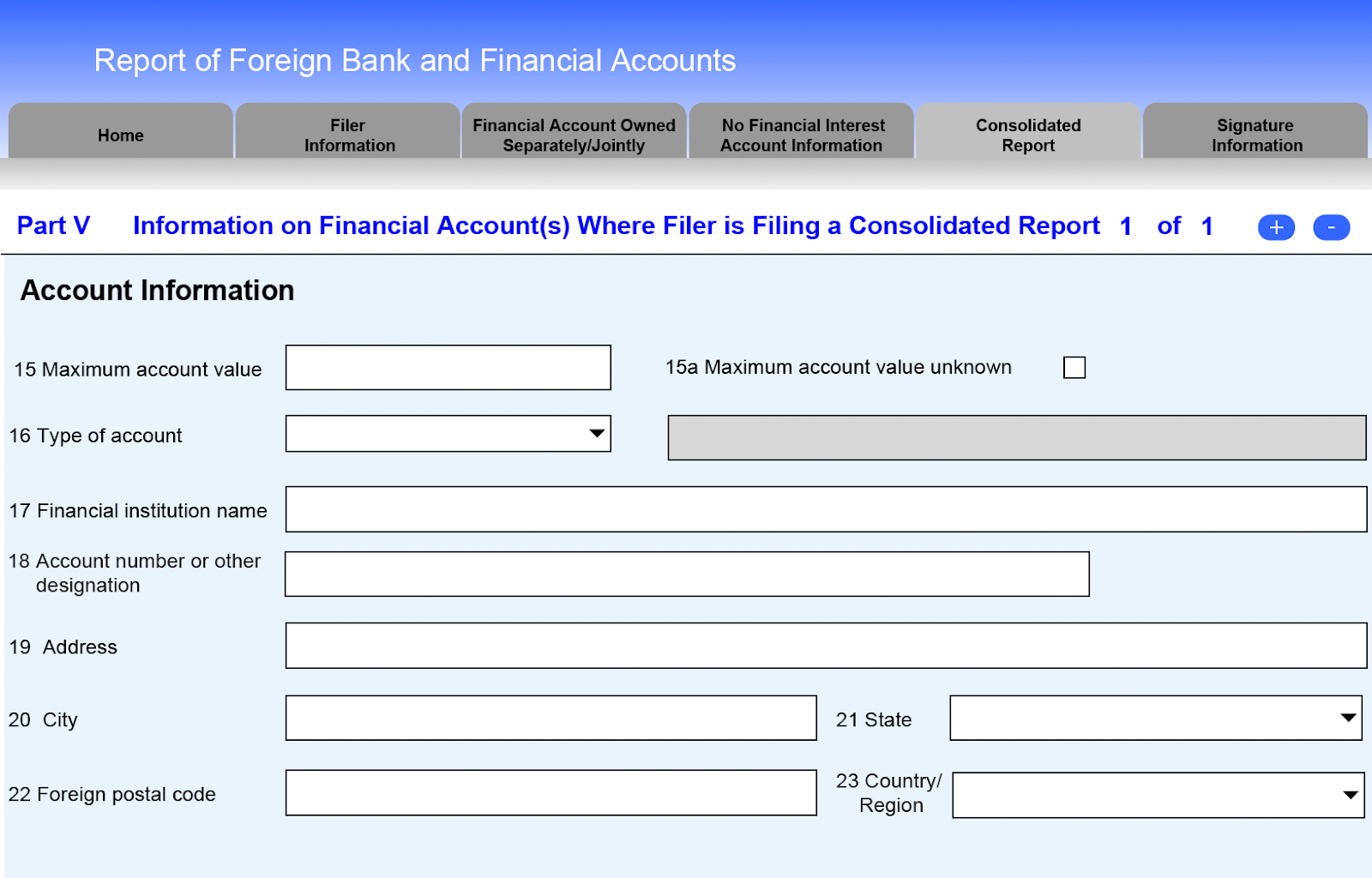

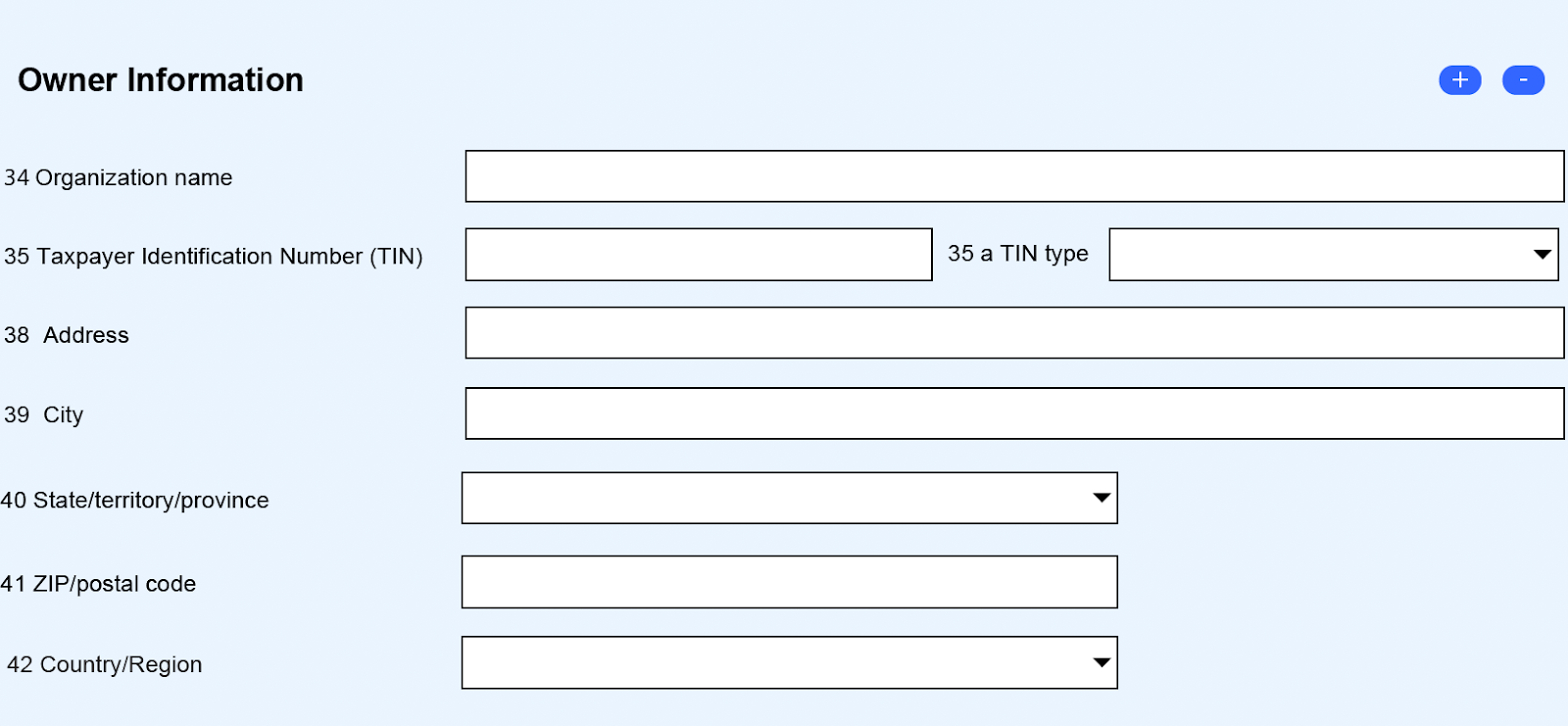

Part V: Information on Financial Account(s) Where Filer is Filing a Consolidated Report

This section is for those who are reporting multiple foreign financial accounts as part of a consolidated report. Typically, this is filed by those reporting on behalf of multiple entities or individuals who have a stake in foreign accounts, such as corporate officers, trustees, or authorized representatives.

Below, you’ll fill out information about the owner of those financial accounts.

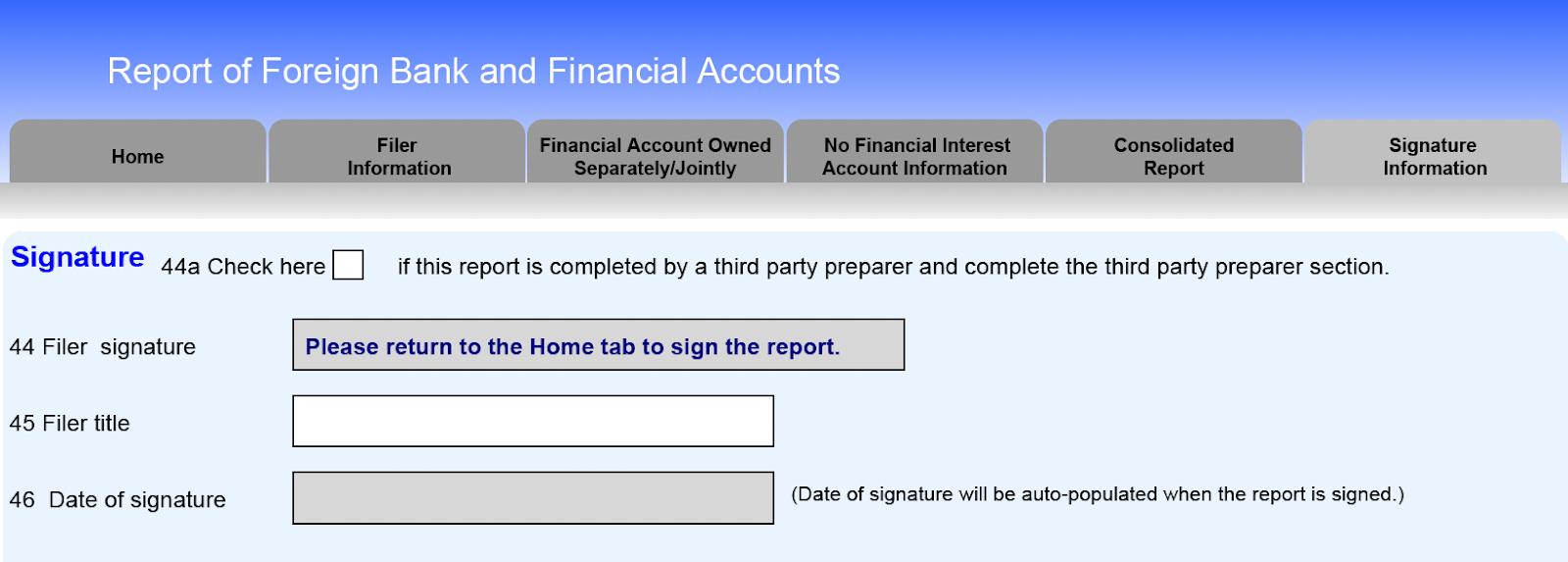

Signature

Finally, you’ll enter your title, the date of signature, and return to the home tab to sign the report. The check box up top is only for third parties preparing your FBAR, such as a tax preparer or enrolled agent.

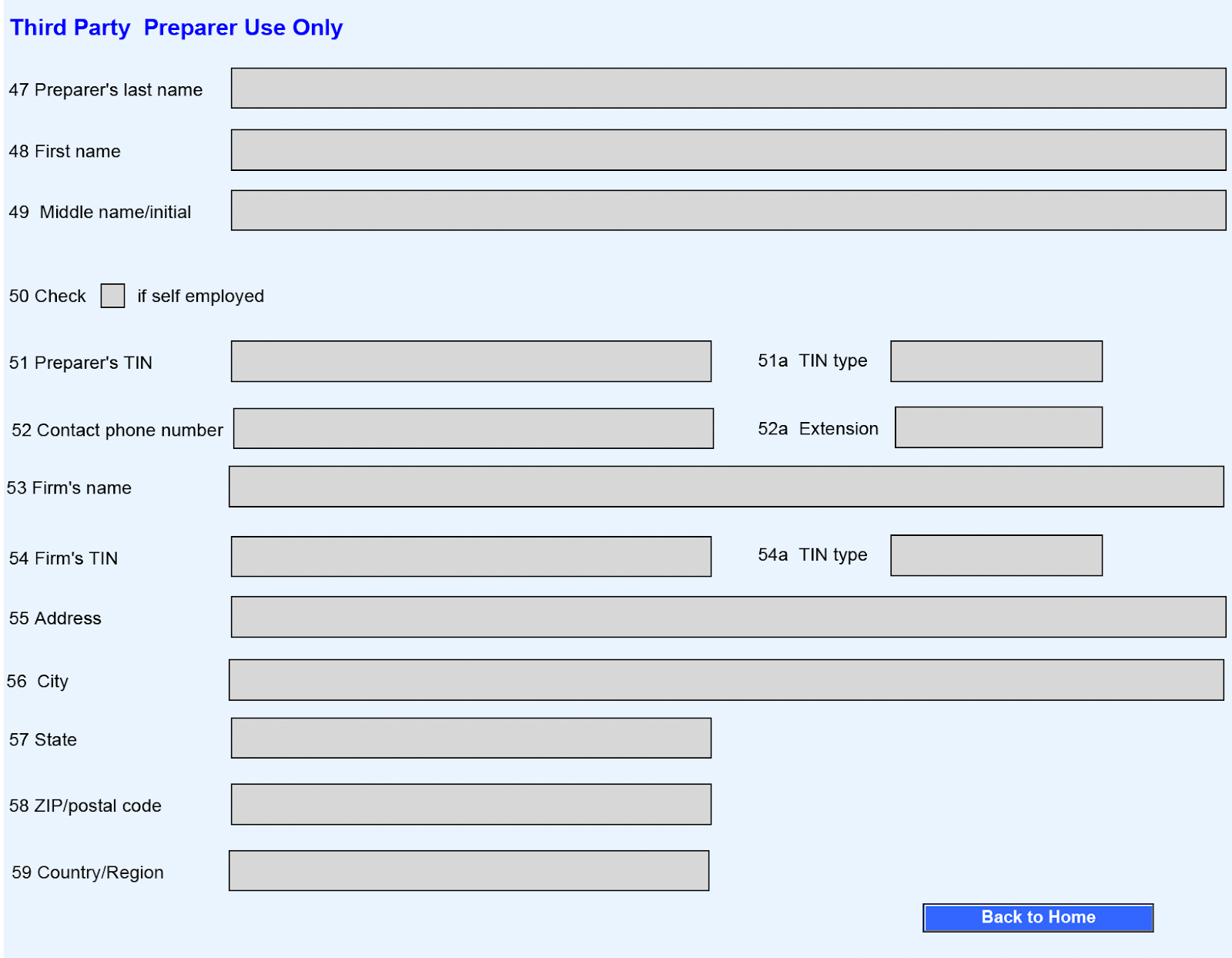

Third party preparers, such as your tax accountant, will also fill out a section at the very end sharing information about themselves or the firm they work for.

FBAR penalties for non-compliance

Unfortunately, even a non-willful (i.e. accidental) failure to file an FBAR when required can result in significant penalties: typically, $10,000 per missed report.

In the case of willful violations, the consequences are even more severe. Someone who willfully fails to file the FBAR faces a penalty of up to $100,000 or 50% of the maximum balance of the account in question in the relevant tax year — whichever’s greater. In extreme cases, someone who intentionally failed to file an FBAR or FBARs can face criminal charges.

You might wonder how exactly the US government can determine whether or not someone has violated an FBAR. After all, how would they know about an American’s foreign financial dealings?

The answer comes back to FATCA, which we mentioned earlier. Beyond establishing Form 8938, FATCA also mandated that foreign financial institutions share information on all of their US account holders. As such, the US Treasury has a similar level of visibility into the foreign financial activities of US taxpayers as they do with their domestic financial activities.

Incidentally, these additional requirements for foreign financial institutions sometimes make it difficult for US expats to open or hold a bank account outside the US.

Catching up on overdue FBARs

If you’re just now realizing that you failed to file FBARs in the past when you should have, don’t panic. The IRS offers a couple of amnesty programs for those who unwittingly fell behind on their tax and reporting obligations, including the:

- Delinquent FBAR Submission Procedure: For those who should have filed FBARs in years past, but did not. The procedure involves filing any outstanding FBARs from previous years along with an attached statement explaining your prior non-compliance

- Streamlined Filing Compliance Procedures: For those abroad who failed to file income tax returns in previous years due to a good-faith misunderstanding of their tax and reporting obligations. Involves filing federal tax returns for the last three years and FBARs for the last six years, if applicable

These programs allow you to get back in good standing with the IRS and FinCEN without having to pay any penalties. To qualify, you must:

- Have fallen behind on your tax and reporting obligations non-willfully (i.e. unintentionally)

- Not be under current IRS investigation

- Take advantage of the programs before the IRS notifies you of your failure to file

Reach full compliance with Bright!Tax

FinCEN Form 114 is essential filing for any expat with $10,000 or more across their foreign financial accounts. The FBAR imposes no tax and helps you avoid major penalties, so there’s no reason not to file it on time. That said, the FBAR is just one of many tax and reporting obligations US expats must keep in mind.

FAQs

-

Can I file an FBAR if I missed the deadline?

Yes — you can and should file an FBAR even if you missed the extended October 15 deadline. Just make sure to explain why you’re submitting late. If you owe an FBAR from previous tax years, it’s better to catch up via the Delinquent FBAR Submission Procedure to avoid penalties.

-

Who qualifies as a “US person” for FBAR purposes?

Here, a US person refers to:

-

- US citizens

-

- Permanent US residents

-

- US-based businesses & entities (LLC, partnership, S Corp, etc.)

-

- US-based estates & trusts

-

- Foreign entities controlled by any of the above

-

-

Does the FBAR threshold change for married couples depending on if they file separately vs. jointly?

No. When it comes to foreign financial accounts, the FBAR threshold is the same whether a couple has filed jointly or separately: $10,000.