Connect on LinkedIn

Connect on LinkedInAs you may already know, moving abroad doesn’t mean you’re off the hook for US taxes. All American citizens and permanent residents who earn above the reporting threshold must file (and pay) US taxes.

If they’re also subject to taxes in a foreign country, they may find themselves reporting same income twice — that’s where tax treaties come in.

The United States has signed tax treaties with dozens of other countries, including the UK, Canada, Australia, and most of the EU. These treaties can help reduce the tax burden for expats and eliminate double taxation (although as we’ll cover below, it’s not always that simple).

To claim the benefits offered by a tax treaty, you’ll need to file Form 8833 with your US tax return. But who can actually claim these benefits, how do you file Form 8833, and what happens if you don’t? We’ll cover all of these questions and more below.

How do tax treaties work?

Tax treaties are agreements between countries designed to avoid double taxation for individuals and businesses who might otherwise be subject to tax in both countries.. They typically:

- Outline which country has the first right to taxation

- Include tiebreaker rules when tax residency is ambiguous

- Offer tax breaks that help eligible beneficiaries reduce their tax liability

In many cases, the benefits enumerated in a treaty can help eligible taxpayers greatly reduce their tax liability or even completely avoid double taxation.

Some tax treaties, for example, exempt certain types of income from US taxation with the assumption that your country of residence will tax them instead. If the tax rate is lower in your county of residence, these provisions are well worth taking advantage of.

Each treaty has different rules and benefits. You can reference the official IRS list of all US tax treaties currently in force for more detail.

The catch for US expats

Unfortunately, tax treaties come with a major caveat for American citizens.

Most tax treaties include a saving clause — a tricky provision which states that the US can tax American citizens as if the treaty never existed. As a result, US expats are generally unable to take advantage of the benefits treaties offer.

That said, most treaties contain exceptions to the saving clause — which allow certain treaty provisions to survive. An exception to the saving clause in the US/UK tax treaty, for example, allows Americans living in the UK to make a one-time, tax-free, lump-sum pension withdrawal.

Certain Americans living abroad temporarily can also typically benefit from tax treaties. This includes:

- Teachers

- Researchers

- Students

- Trainees

Keep in mind that certain states do not honor international tax treaties, like California, New Jersey, Pennsylvania, and others. So, even if you qualify for a tax treaty’s benefits on your federal return, those same benefits won’t necessarily apply to your state return.

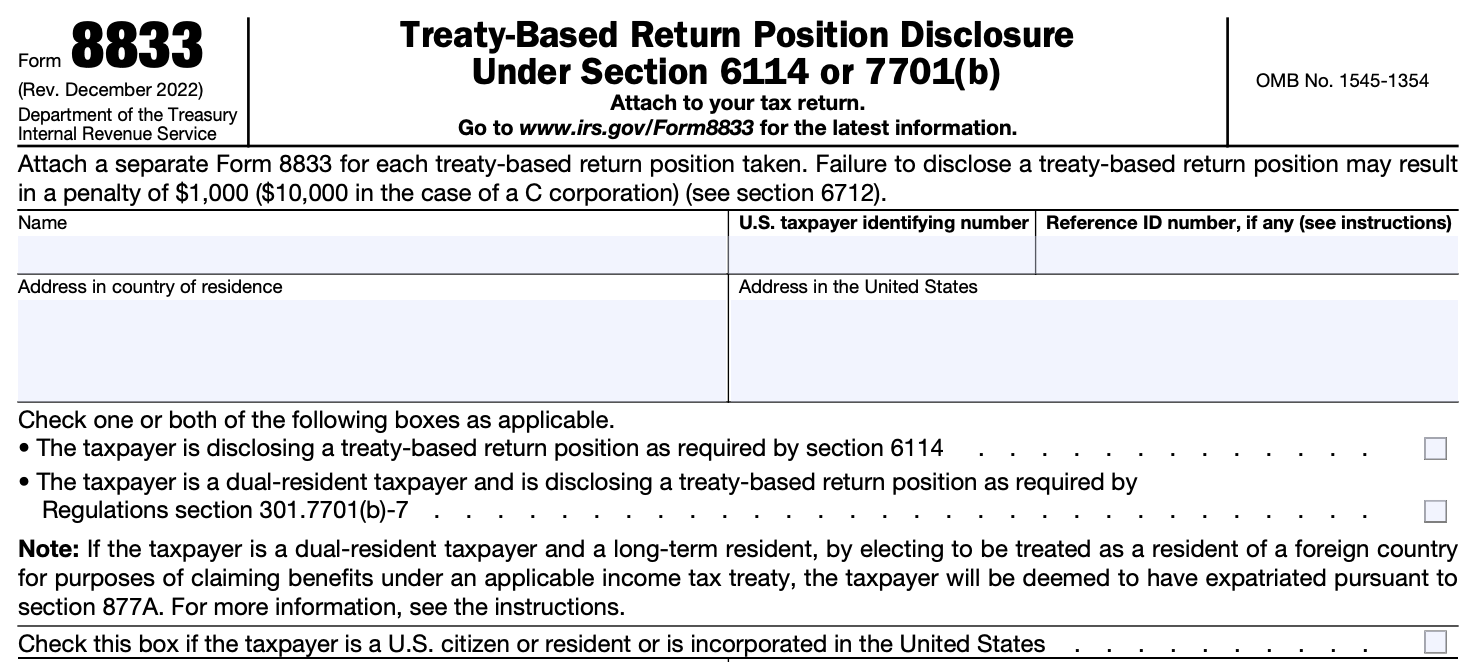

What is Form 8833?

Form 8833: Treaty-Based Return Position Disclosure Under Section 6114 or 7701(b) is the form you’ll use to claim tax treaty benefits. Each year you want to capitalize on a tax treaty, you must complete Form 8833 and include it with the rest of your tax return.

How do I file Form 8833?

The good news for taxpayers who file Form 8833 is that it’s just one page long.

In the first half of the document, you’ll start by entering basic information like your name, taxpayer identifying number (usually your SSN), and address(es).

Then, you’ll need to check boxes if you are claiming a treaty provision, a dual-resident taxpayer, or an American citizen or resident.

B!T related: Dual Citizenship Taxes: A Guide for US Expats

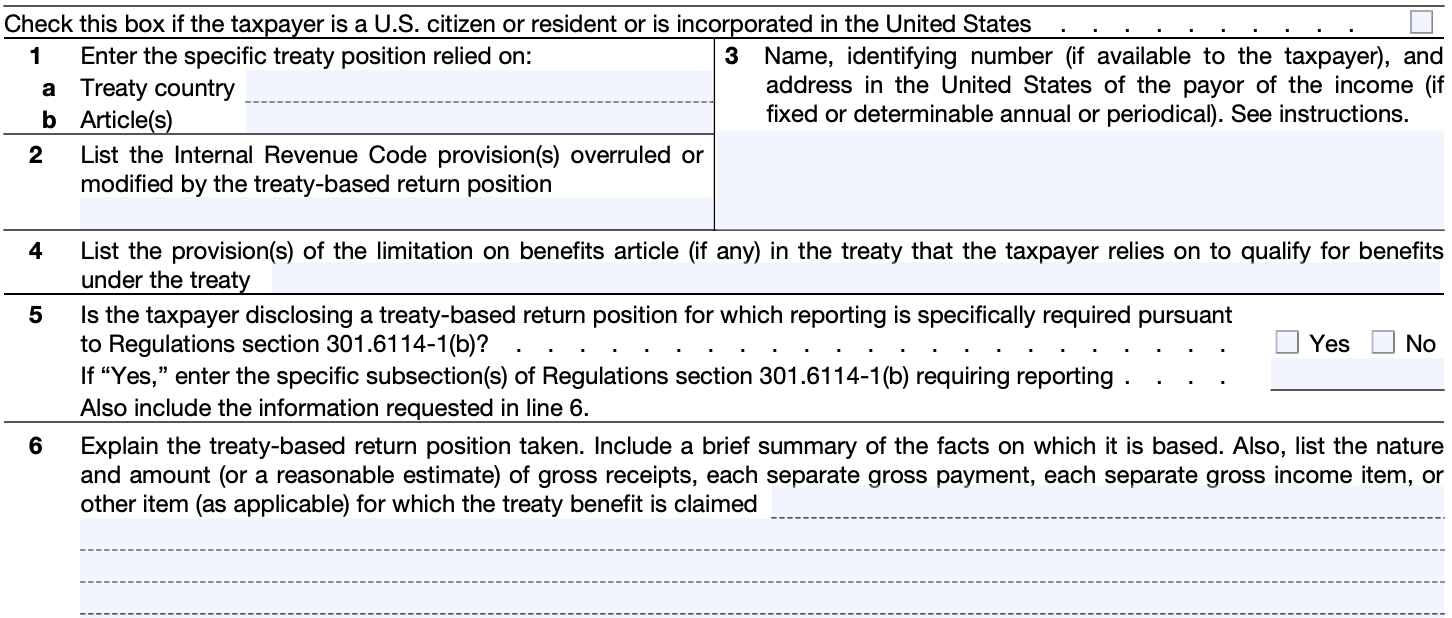

In the second half, you’ll get more specific about which treaty benefit you’re claiming. This requires you to:

- Cite the specific treaty article that contains the benefit you’re claiming

- Indicate which limitations apply to the benefit, if any

- Explain how the treaty benefit applies to your situation and list which income it applies to

B!T note: If you plan on claiming more than one treaty benefit, you’ll have to file a different Form 8833 for each benefit you claim.

As you can imagine, this can all get fairly technical. If you’re not used to interpreting and referencing complex legal documents, you may want to hire a tax preparer to complete it on your behalf.

You can file Form 8833 either electronically or by mail.

Are there penalties for failing to file IRS Form 8833?

If you don’t claim a tax treaty benefit on your return, you won’t need to file Form 8833, so there will be no penalties for noncompliance. But if you do exclude income based on a treaty benefit without filing Form 8833, you are subject to a fine of $1,000.

In some cases, the IRS may waive these fees if you can provide a reasonable explanation of why you didn’t file Form 8833.

In a few cases, individuals are exempt from having to file Form 8833 after claiming a tax treaty benefit.

Who is exempt from filing Form 8833?

According to the IRS, you don’t have to file Form 8833 if you:

- Claim a reduced withholding tax under a treaty on interest, dividends, rent, royalties, or any other fixed or determinable annual or periodic income typically subject to a rate of 30%

- Claim a treaty exemption that results in reduction or modification of taxable income from:

- Dependent personal services

- Pensions

- Annuities

- Social security

- Are a partner in a partnership or a beneficiary of an estate or trust, and that partnership, estate, or trust reports that required information on its return

- Qualify to claim a reduction or modification of the taxes applied to income under an International Social Security Agreement or a Diplomatic or Consular Agreement

- Declare payments or items of income that don’t surpass $10,000

Avoid double taxation with an optimized return

It’s certainly worth looking into whether or not you can claim tax treaty benefits on your annual US tax filing. If you do, you’ll have to file Form 8833 — but you may need help from a tax professional to help navigate the complexities. Keep in mind, though, that saving clauses prevent most US expats from claiming the vast majority of tax treaty benefits.

However, that doesn’t automatically mean you have to pay double taxes. There are other tools you can use to mitigate your US tax liability, like the Foreign Earned Income Exclusion (FEIE) and the Foreign Tax Credit (FTC).

Form 8833 FAQs

-

What is the difference between Form 8833 and Form W-8BEN?

While both forms have to do with tax treaty benefits, they serve different purposes. Form 8833 is for US tax residents claiming international tax treaty benefits on their tax return.

Form W-8BEN, on the other hand, is for nonresident individuals, entities, and investors with certain types of US income. Filing Form W-8BEN allows these groups to potentially claim reduced withholding tax rates and other treaty benefits as applicable.

-

What is a nonresident alien?

A nonresident alien is a foreign national subject to US taxes but who does not meet the “resident alien” definition. To qualify as a resident alien, you must meet one of two tests:

- The Green Card Test: Hold a green card

- The Substantial Presence Test: Have spent over 183 days in the US over the past three years, counting:

- All the days in the current year

- ⅓ of the days last year

- ⅙ of the days two years ago

-

Who may qualify for the Foreign Tax Credit?

The Foreign Tax Credit (FTC) gives eligible taxpayers dollar-for-dollar US tax credits for any foreign taxes they’ve paid. They can then apply these credits toward future US tax bills up to 10 years afterward. To qualify, the taxes must be:

- Legal

- Based on income

- Due by you specifically

- Paid or accrued