Connect on LinkedIn

Connect on LinkedInIt may not be a well-known tax form, but Form 3520 is essential for many US expats. It’s mandatory for Americans affiliated with foreign trusts or who have received certain foreign gifts. Those who fail to file it when required fall short of tax compliance and can face significant penalties.

Although Form 3520 can be complex, we have plenty of experience with it as a tax firm specializing in US expat taxes. Below, we’ll walk you through who must file Form 3520, how to do so, where to send it, and more.

What is Form 3520?

It’s fairly evident from its full title — Form 3520 (Annual Return To Report Transactions With Foreign Trusts and Receipt of Certain Foreign Gifts) — what Form 3520 is for.

Like the Foreign Bank Account Report (FinCen114) or Statement of Specified Foreign Assets (Form 8938), this form gives the US government visibility into Americans’ foreign financial dealings. In turn, this helps the US enforce international tax compliance and reduce the risk of offshore tax evasion.

When to file Form 3520

Form 3520 reporting is necessary for US taxpayers — individuals, corporations, partnerships, and estates — who are either:

- Owners of a foreign trust

- Beneficiaries of a foreign trust

- Responsible parties for a foreign trust (such as, in charge of administering, overseeing or reporting on the foreign trust’s behalf) or

- Recipients of certain gifts or bequests from foreign persons, estates, corporations, and partnerships

Depending on the amount, those who receive gifts or bequests from foreign persons, estates, corporations, and partnerships may not need to file Form 3520. We’ll discuss that later.

Domestic trusts vs. foreign trusts

It’s worth clarifying how exactly the Internal Revenue Service (IRS) defines a foreign trust. The IRS considers a trust to be domestic if a US court has primary supervision over the trust’s administration and one or more US persons control all the main decisions relating to the trust. They consider all other trusts foreign.

The IRS will always view a trust set up in a foreign country as a foreign trust, even if all the owners and beneficiaries are American and the trust’s assets are in the US.

How to File Form 3520

Many people wonder, can Form 3520 be filed electronically?

Unfortunately, it cannot (and neither can 3520-A). While the IRS briefly allowed people to file Form 3520 online during the pandemic, you must now complete, print, and mail a physical copy to the IRS.

That said, a tax professional can file the form on your behalf, so you don’t have to mail it personally.

Form 3520: Step-by-Step

Now that we’ve gotten through the context let’s move on to exactly how to complete Form 3520.

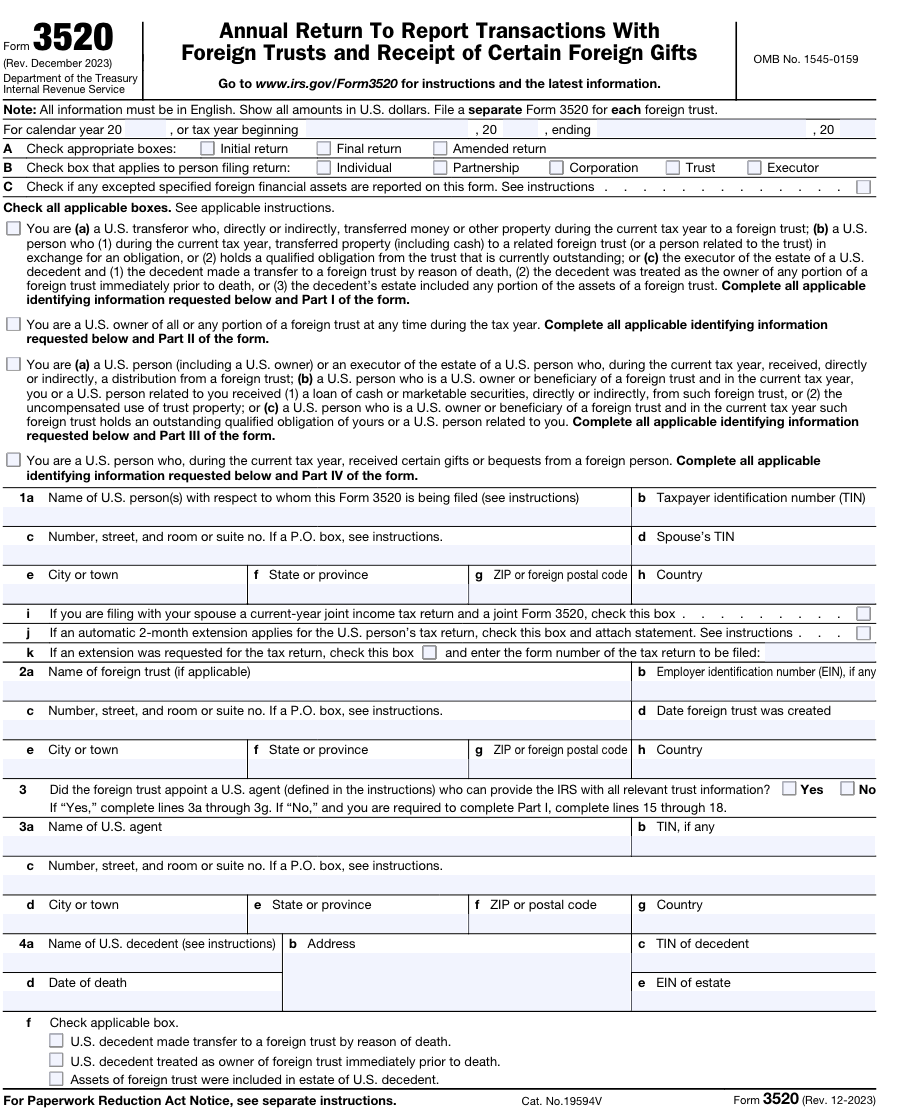

Basic information

In the first section of the form, you’ll enter basic information such as:

- The calendar year you’re filing for

- Whether you’re filing for the first time or amending an existing return

- What type of entity you’re reporting for, which is generally Individual for a US taxpayer

The next section with checkboxes will help you determine which parts of the form you must complete.

Pro tip:

When reporting foreign currencies, you should always convert values into US dollars using a reliable IRS-approved source, like Google, XE, or Oanda.

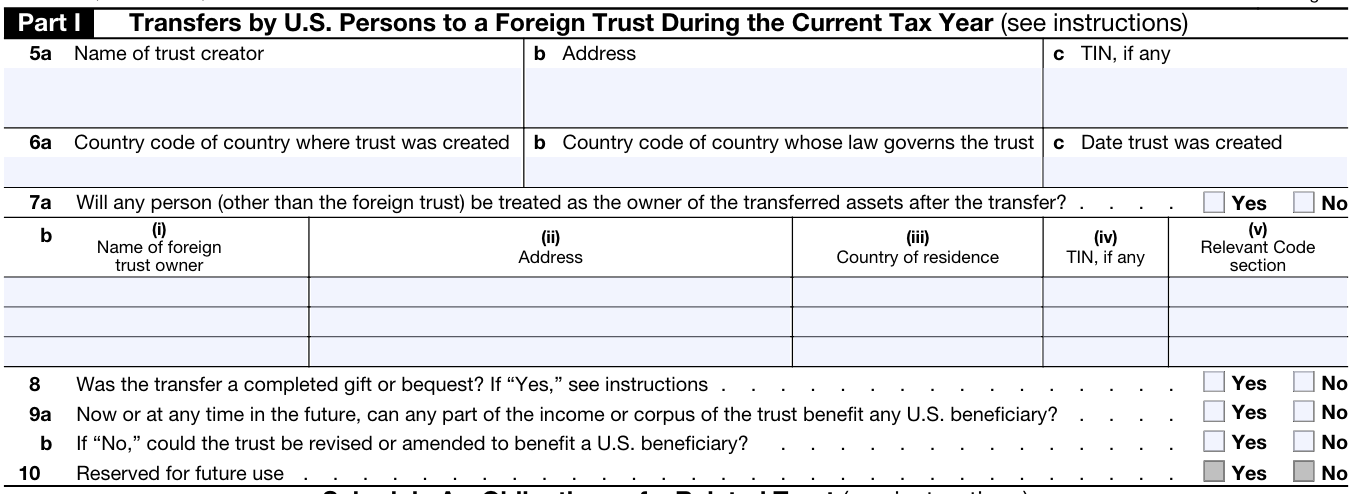

Part I: Transfers by US Persons to a Foreign Trust During the Current Tax Year

The first part of the form is for people who met at least one of the following criteria in the last tax year:

- Have made transfers of property (cash, stock, bonds, loans, etc.) to a foreign trust or person affiliated with a foreign trust

- Are responsible for overseeing or reporting a foreign trust’s reportable events

- Are the executor of a US state that made a transfer to a foreign trust or a person who held ownership in a foreign trust

You’ll start by sharing information about the trust creators and owners, and answer yes or no questions about transactions and beneficiaries.

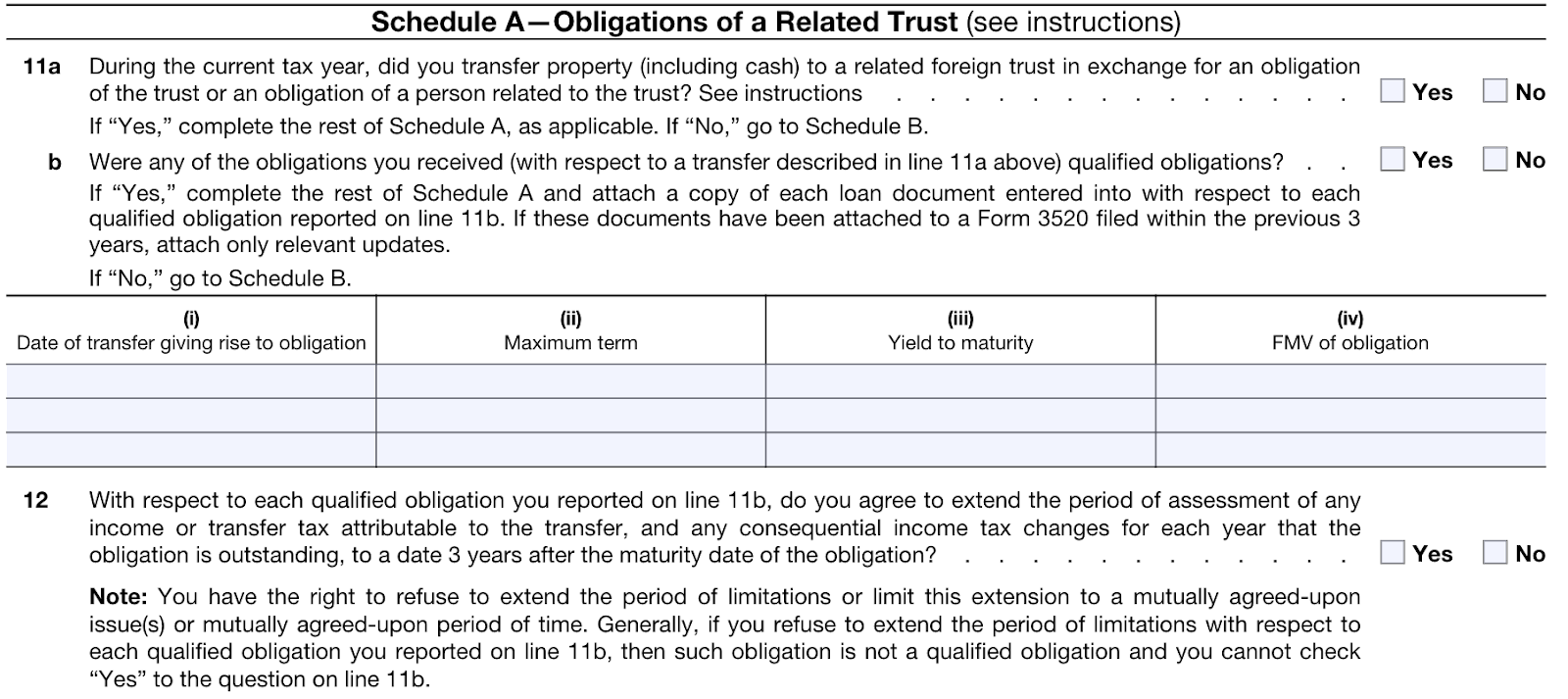

Schedule A: Obligations of a Related Trust

This section is for those who have transferred property to a foreign trust in exchange for an obligation, such as a loan. Again, you’ll answer a few yes or no questions then share details of any relevant transfers.

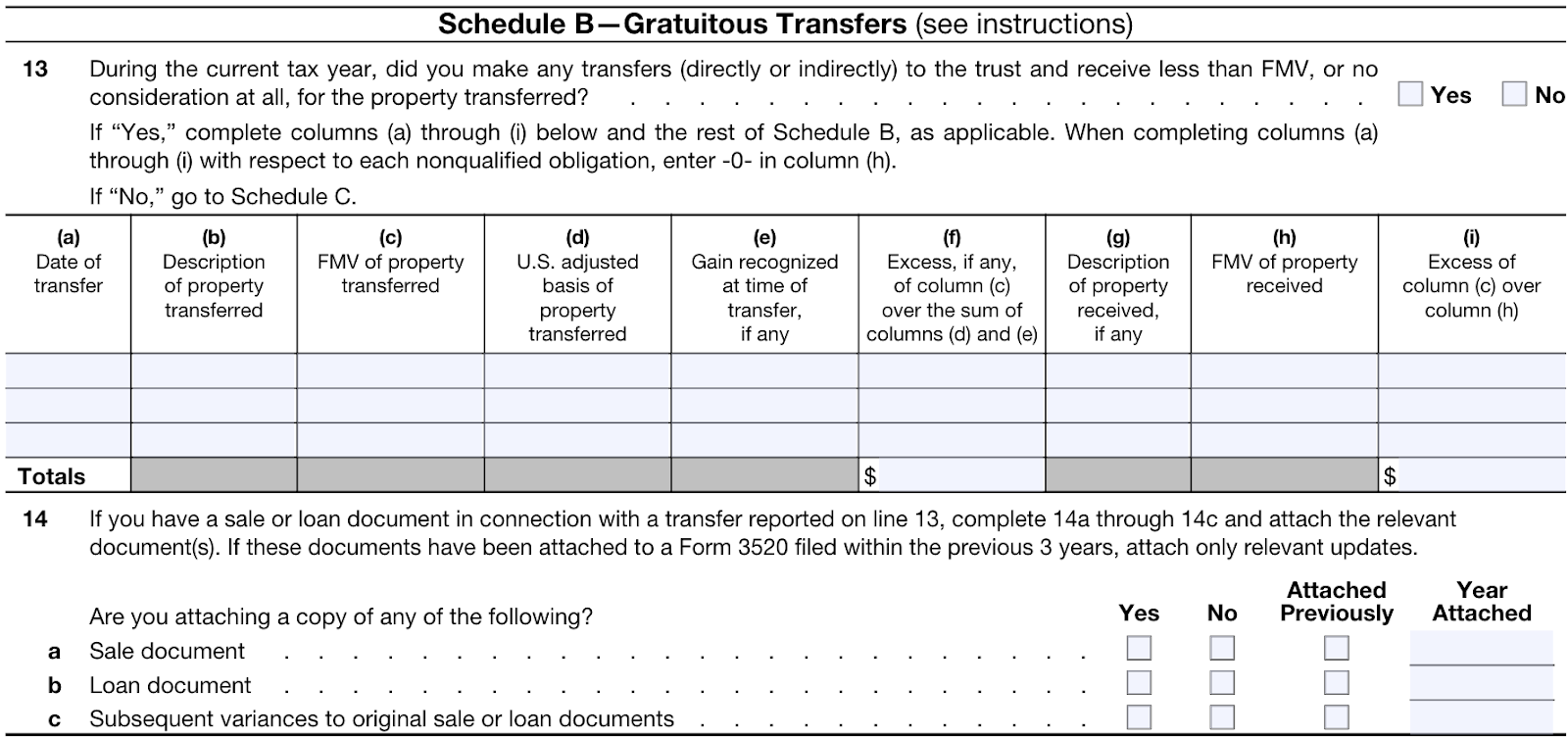

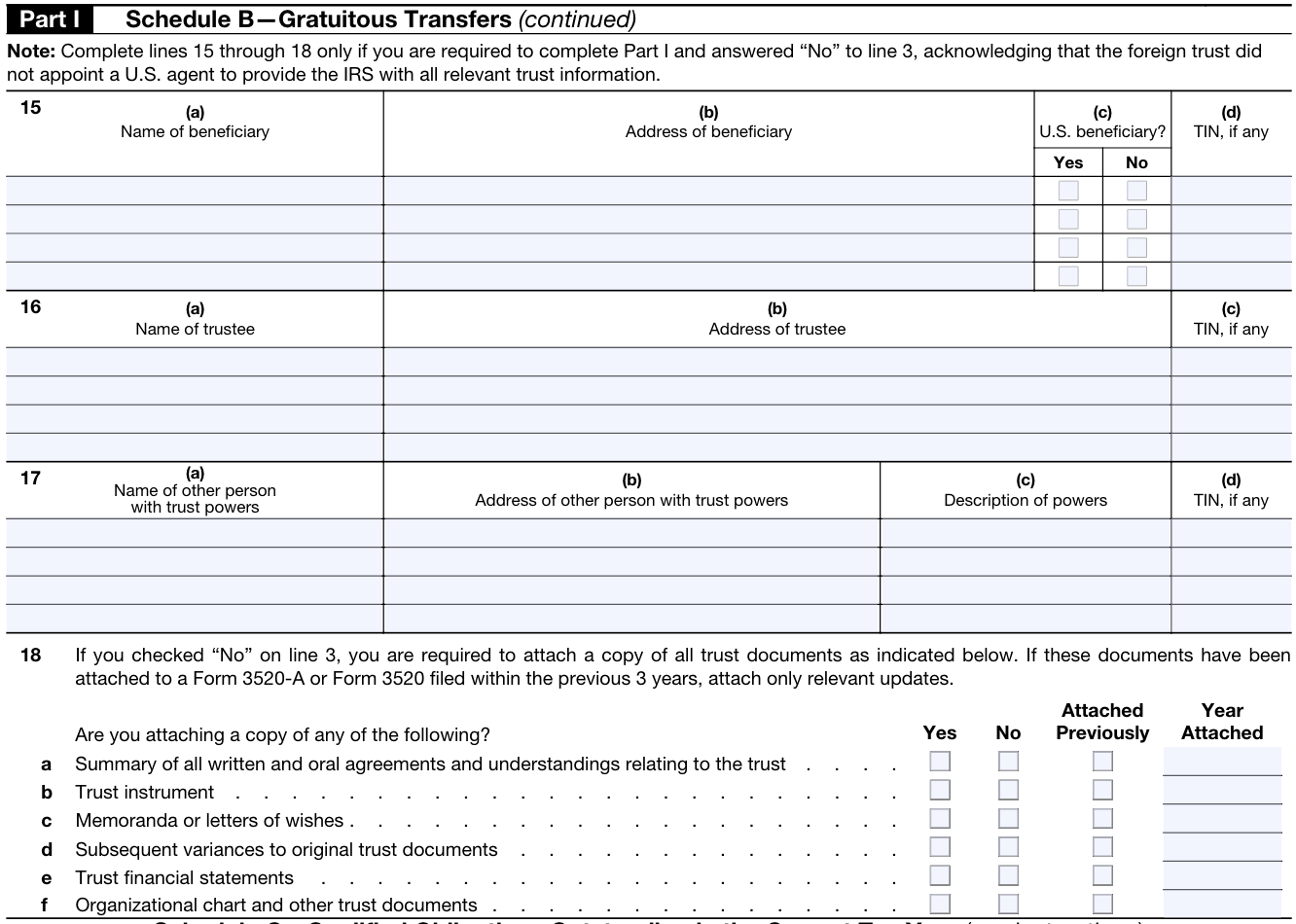

Schedule B: Gratuitous Transfers

Schedule B of Part I is for “gratuitous transfers,” or transfers in which the transferor receives less than the fair-market value of the property transferred in return.

If the foreign trust hasn’t already appointed a US agent to share relevant information with the IRS, you’ll need to complete lines 15 through 18, sharing details on:

- Beneficiaries

- Trustees

- Other people with trust powers

- Certain official trust documentation

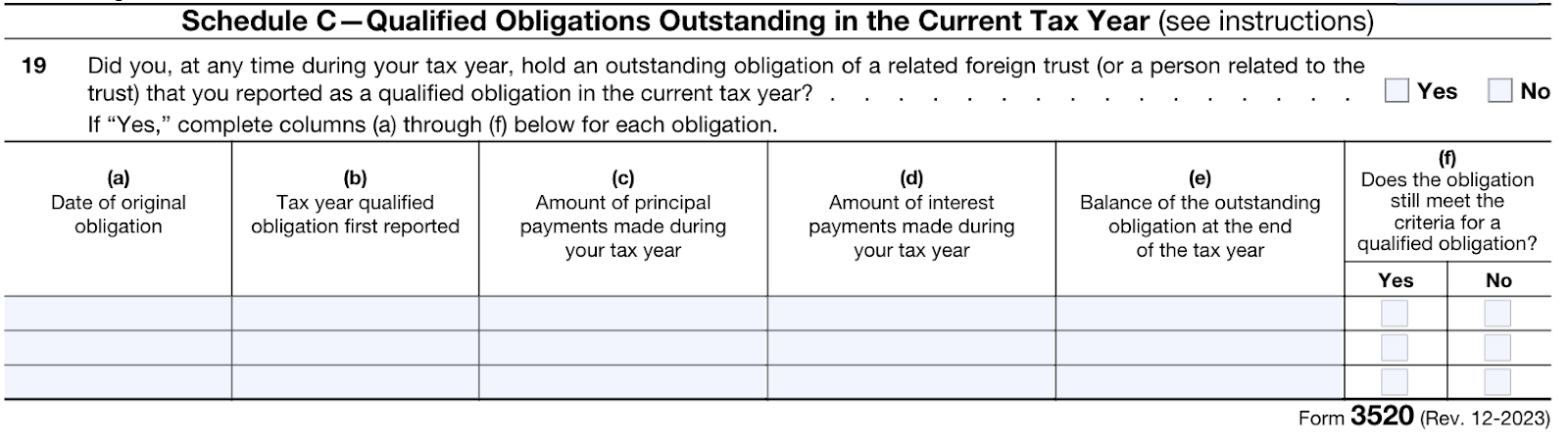

Schedule C is for those responsible for overseeing or reporting reportable events of a foreign trust. In it, they’ll share details on any obligations (typically loans) they hold in relation to a foreign trust or person related to a foreign trust, such as when the event occurred, when it was reported, and how much interest they’ve paid on it.

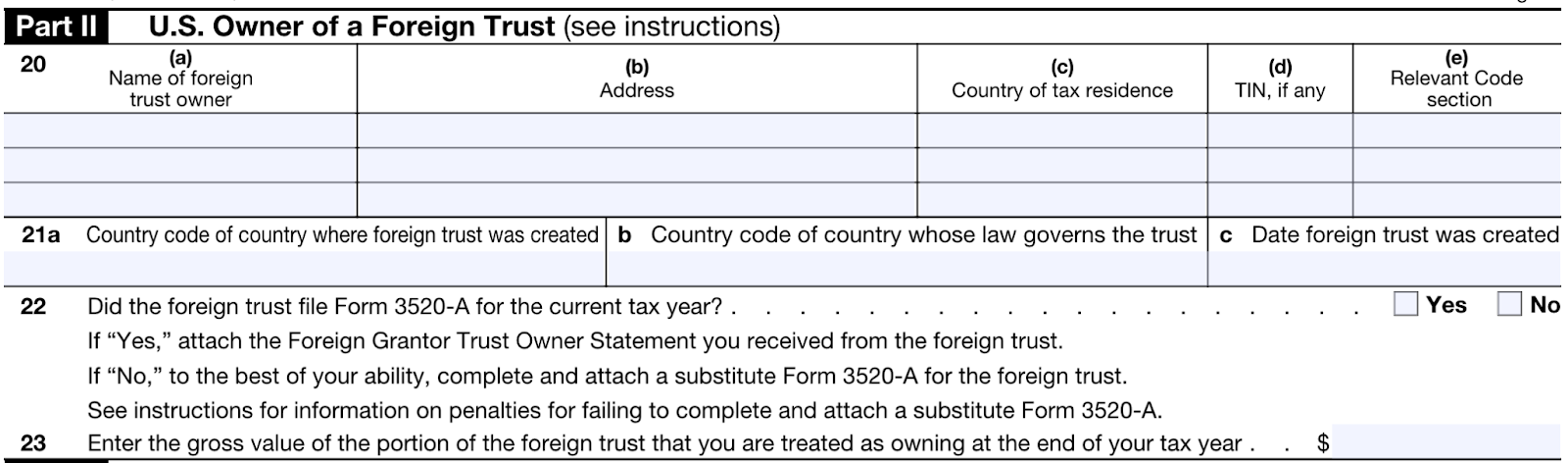

Part II: US Owner of a Foreign Trust

As its name implies, Part II is for Americans who own a foreign trust in whole or in part and hold certain powers or interests in it (aka a grantor trust).

It’s important to note that IRS regulations may consider the US beneficiaries of foreign trusts to be owners as a result of their interest in the trust, by default, and as such this section may be relevant to US beneficiaries as well.

For example, let’s say that Ted creates a foreign trust for tax purposes and transfers $1,000,000 into it. He can choose to revoke or receive at any given time, so he still holds an interest in it. As such, he must fill out Part II.

In this section, you’ll share information about the foreign trust and its owner, such as the owner’s name and address, the country where the trust was created, and the date on which it was created. Note that having to fill out Part II also immediately triggers a requirement to fill out Form 3520-A.

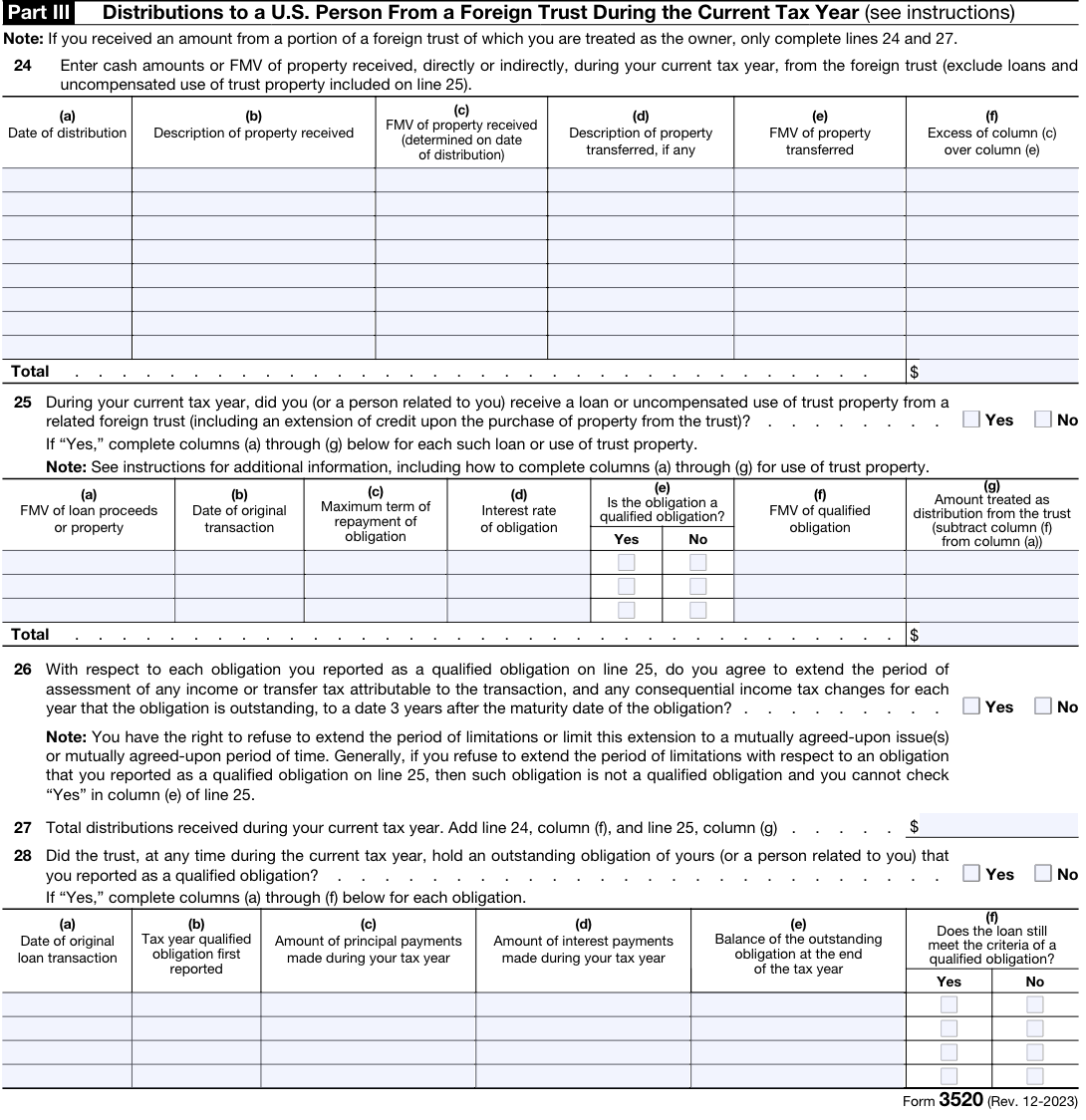

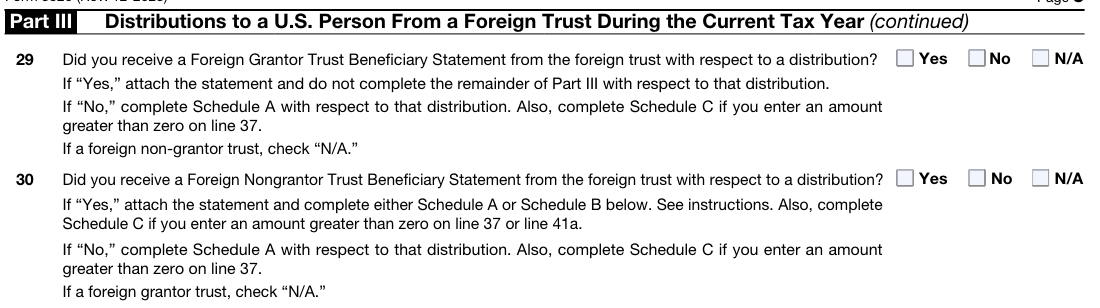

Part III: Distributions from a Foreign Trust

In Part III, you’ll report any distributions — both direct and indirect — you received from a foreign trust. Here, a distribution refers to any transfer of property made by a foreign trust to an American taxpayer recipient (including cash, real estate, stock).

This encompasses both distributions made directly from the trust to the taxpayer and indirect distributions, like payments to a company controlled by an American taxpayer.

Let’s say Sadie owns an S Corp and provides business consulting services for a Japanese company owned 100% by a Japanese trust. The trust makes a payment to her S Corp rather than to her directly, which qualifies as an indirect distribution. As both direct and indirect distributions from foreign trusts are subject to reporting, she must file Form 3520.

Note:

While both direct and indirect distributions are subject to Form 3520 reporting, they may have different tax implications depending on the income and trust type.

After providing details of the distributions (date of receipt, type of distribution, fair market value), you’ll answer some yes or no questions about the foreign trust’s obligations and documentation.

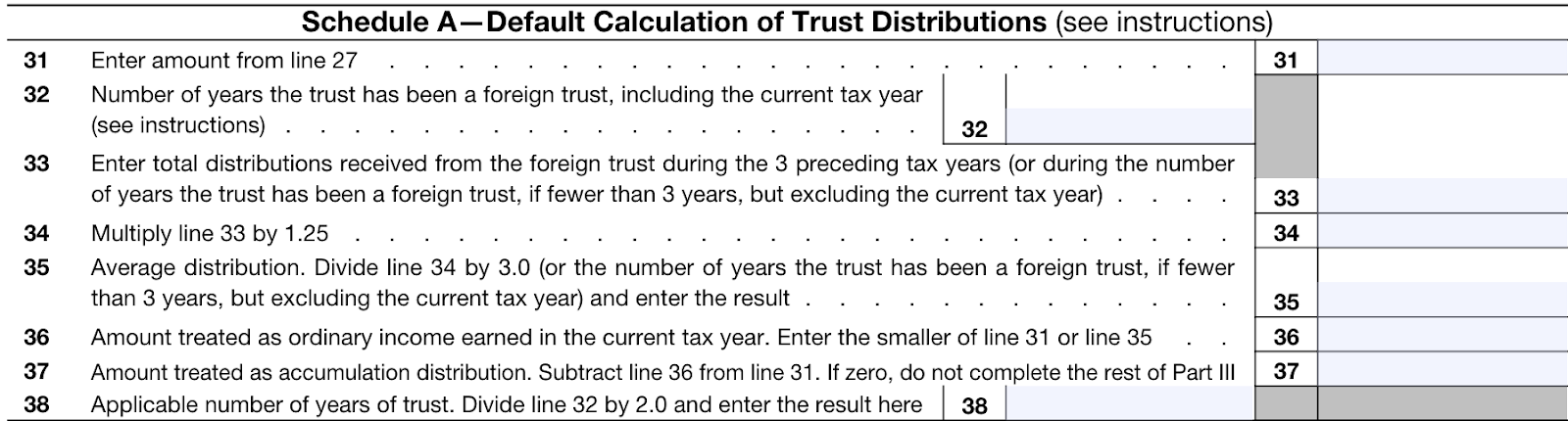

Schedule A: Default Calculation of Trust Distributions

In Part III Schedule A, you’ll calculate how much of your distributions — if any — are subject to reporting on your individual tax return.

Pro tip:

If you paid taxes on foreign trust distributions in another country, you may be able to use the Foreign Tax Credit (FTC) to claim dollar-for-dollar US tax credits for those payments.

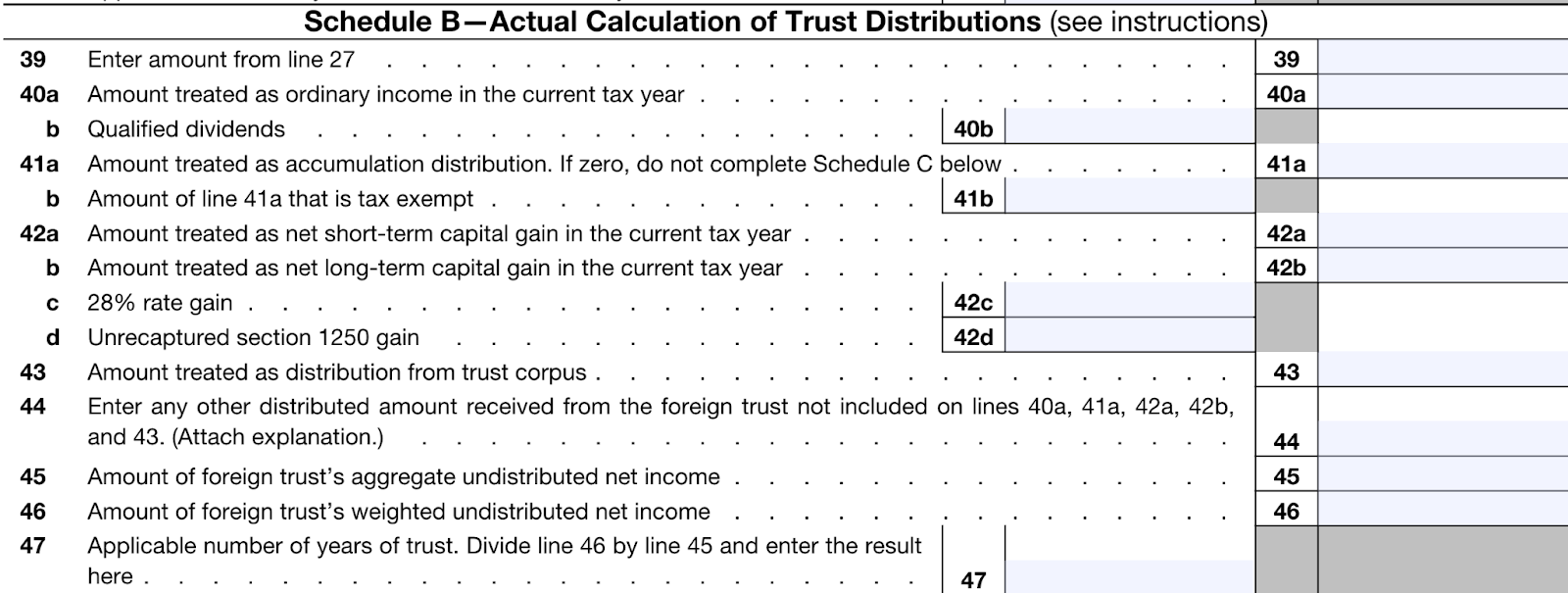

Schedule B: Actual Calculation of Trust Distributions

In Schedule B of Part III, you’ll break down the trust distributions into different categories of income.

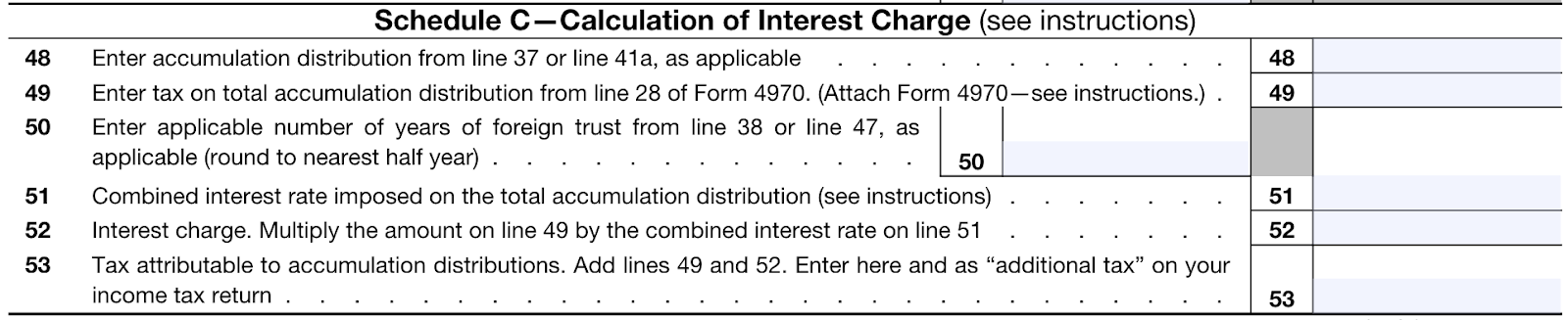

Schedule C: Calculation of Interest Charge

Schedule C of Part III requires you to calculate whether you owe any taxes associated with interest on the accumulation distributions you’ve received (which is different from the calculation of the tax itself, calculated on your tax return, such as 1040).

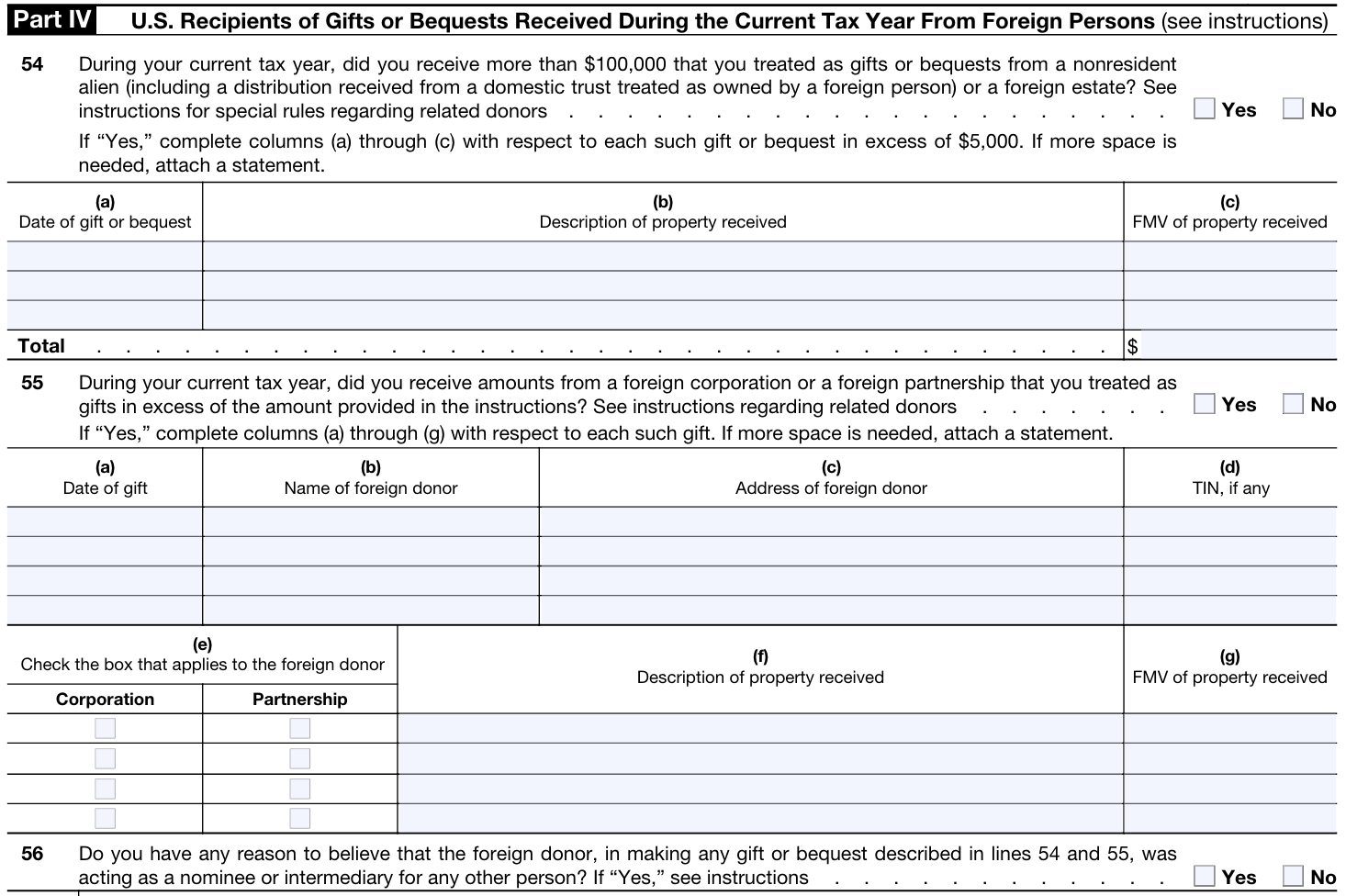

Part IV: Receipt of Certain Foreign Gifts

Part IV of Form 3520 is mandatory for those who have:

- Received gifts of over $100,000 from foreign persons or estates

- Received gifts or bequests exceeding the annual reporting threshold ($18,567 for tax year 2023, $19,570 for 2024) from a foreign corporation or partnership

- Note: This threshold increases slightly each year to account for inflation

These groups will use lines 54 and 55 (as relevant) to share details on each gift or bequest, like when they received it, what it consisted of, and what the fair market value was. They’ll use line 56 to indicate whether or not the foreign donor was acting as an intermediary (say, the executor of someone’s will, a family member, or a legal representative).

Signature

Last but not least, you’ll sign the form to certify under penalty of perjury that the information above is correct. If you paid someone to prepare the form for you, they’ll have to sign and share some personal information as well.

When is Form 3520 due?

You’ll need to file Form 3520 along with Form 1040 and the rest of your federal tax return. While most Americans think of April 15th as the typical tax deadline, US expats get an automatic two-month extension to June 15th. If you need more time to file, you can apply for an additional extension to October 15th.

Note:

If any of these days falls on a weekend, the deadline changes to the next business day afterward. Keep in mind, though, that you must still pay any taxes you owe by the standard April 15th deadline.

Where to mail Form 3520

Once you’ve completed Form 3520 and the rest of your tax return, it’s time to mail it in. Where to send Form 3520 will depend on whether you’re attaching a payment (check, money order) along with it.

If you won’t be attaching a check or money order, send your return to:

Department of the Treasury

Internal Revenue Service

Austin, TX 73301-0215

USA

If you will be attaching a check or money order, send your return to:

Internal Revenue Service

P.O. Box 1303

Charlotte, NC 28201-1303

USA

Additional considerations

A few other things to keep in mind when it comes to Form 3520 include:

- Form 3520-A: As we mentioned earlier, foreign grantor trust rules require US owners of such trusts to file Form 3520-A (Annual Information Return of Foreign Trust With a US Owner) in addition to Form 3520. Notably, you must submit this form by March 15th — before you submit the rest of your tax return

- Penalties for non-compliance: Not filing Form 3520 when required could result in significant penalties, such as:

- 35% of gross property value transferred to a foreign trust if the creation of that trust wasn’t properly reported

- 35% of the gross value of the foreign trust distributions made but not properly reported

- 5% of the gross value of assets of the owner in the foreign trust if said owner didn’t properly disclose their ownership

- Professional assistance: When it comes to tax returns, you want to get things right the first time. If you’re unsure about anything, don’t hesitate to contact a licensed tax preparation professional

Get help with Form 3520 & beyond

If you own, receive property from, or are otherwise affiliated with a foreign trust, you may very well need to complete Form 3520. Filing it completely and accurately is essential to compliance, and failing to do so can come with steep penalties.

Resources:

- Large gifts or bequests from foreign persons

- Gift Tax, Explained: 2024 Exemptions and Rates

- TFSAs for U.S. citizens: might be worthwhile with some caveats

Form 3520 FAQs

-

How much money can be gifted tax-free in the US?